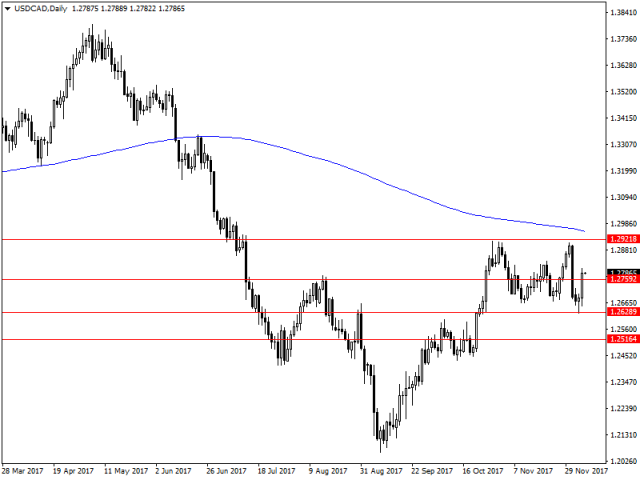

The Canadian dollar was back in focus today as the market was looking for hawkish signs from the Bank of Canada, on the back of the recent interest rate statement. The interest rate was kept at 1% however, and the market was caught off guard by the dovish comments made by the BoC. While the economy has been adding new jobs and Fridays figures were a testament to that (+441,400), the BoC is still concerned about the NAFTA negotiations that are ongoing, as well as recent housing market developments. This came as a shock for a lot of market pundits, but more important it forced forecasts further out for future rate rises, while before the market was betting heavily on the BoC to come through and cause further positive betting on rate rises.

The USDCAD was quick to jump on the back of the news out from the BoC, as USD bulls rushed away with all the recent gains and pushed through resistance at 1.2759. Further levels higher can be found at 1.2921 with the potential for any higher gains to the 200 day moving average - which would be very hard to push through. If the market does turn around and head back south then support at 1.2628 and 1.2516 are likely to be the prime candidates for bearish traders, with the area between these two levels likely to act as a key selling point on the market.

Crude has been one of those funny players in the market as of late with a bullish rise, which has been purely on the back of OPEC extending production cuts. Now for many this comes as no surprise as the oil market did need to stabilise but today's fall caught many off guard given that the drawdown came in stronger than expected at -5.61M (-2.5M exp). The reason for this was refined oil products with gasoline showing an increase to 6.8M barrels, beating market expectations and causing the oil market to sell-off. Selling pressure is common when you have a build up of refined products as the market might start to think it's flagging or peaked already.

Oil now finds itself in a weird place at present as the recent rise has struck strong resistance at 59.08 in this market, and the fall today hit the current old trend line which the market is respecting before taking a pause and stopping all together. I'm not sure if there is further potential falls on the cards given the bulls have been so strong, and this could be an excuse to unwind. However, if the trend line did break then support could be found at 55.14. If oil does indeed jump back higher, then for me resistance at 57.38 and 59.08 are the key levels traders will look to target. Expectations are though that 59.08 will be the level to beat currently.

Daily Fundamental ForexTime ( FXTM )

Bitcoin future trading kicks off; Investors awaiting central banks decisions

Trading bitcoins entered a new phase today, after Chicago’s CBOE listed the first futures contract on the cryptocurrency. The initial reaction was beyond expectations with the futures contract climbing more than 20% and triggering two trading halts. CBOE’s website experienced unprecedented traffic which may well have sent a new benchmark, the frenetic activity lead to delays and outages. So far, it seems professional investors aren’t willing to bet against the bitcoin, despite the many warnings of a bubble that will burst soon. Many traders aren’t even interested in the price direction, but the listing of the futures contract on CBOE and later next week on the CME, will provide them an arbitrage trading opportunity due to the vast pricing differences. However, the arbitrage trading will lead to improved price efficiency and probably less volatility. After volatility settles down, the focus will return to the price direction.

Central Banks Meetings

Currency markets were trading in tight ranges early Monday with the dollar slightly weaker against its major peers. Expectations of the Fed hiking rates on Wednesday, stands at 90.2% according to CME’s Fedwatch tool which means the disappointment in wage growth won’t shift the needle for US monetary policy. However, it isn’t the rate hike that will move the dollar on Wednesday, it’s the tone, economic projections and the dot plot. Given that we’re getting closer to a deal on tax reforms, the Fed might become slightly more hawkish. It remains to be seen whether this will shift up the Fed’s dots for future interest rate expectations.

The European Central Bank and Bank of England are also meeting this week. Despite no substantive monetary policy changes expected, the language might still move the Euro and the Pound.

Will the Fed support further rotation in stocks?

Tech shares have been in focus over the past two weeks after the S&P tech index plunged more than 4% between 29-Nov and 05-Dec, before recovering last week. The fall in Teck stocks wasn’t accompanied by a selloff in other sectors, particularly the financials which have been on the rise. This is a classic type of rotation with active managers balancing their portfolios before year end. Tax reforms don’t seem to be of great support to Tech firms, given that their effective tax rate is considered to be the lowest in the U.S. Meanwhile, it’s a big deal for the rest of the U.S, with financials having an effective tax rate of more than 30%. The new Fed Chair, Jerome Powell will likely speed up deregulation for the financial sector which will drive more inflows. And of course, higher interest rates for 2018 will further support the banks' profit margins. That’s why the trajectory of interest rates in 2018 will likely lead to more portfolio balancing before year end.

EU Summit

The breakthrough in Brexit talks on Friday was a great relief for policymakers, who can now move to phase-2 of the talks. Interestingly though, Sterling instead of rising sharply, dropped on the news. Investors seem reluctant to buy Sterling as they view the next phase more complicated than the first. They want to see details of the transition agreement and trade talks concluded before buying Sterling. I don’t think the EU summit on Friday will reveal much, but blessings from EU leaders might lend some support to the Pound.

For the Bank of England's Mark Carney today was not his day as inflation once again lifted to 0.3% m/m and 3.1% y/y (3.0% exp), which in turn meant that being above the 2% inflation target he was obliged to write a letter to the Chancellor of the Exchequer to explain why it's so high. In the modern age with all in the information that seems somewhat silly, but the reality is that Brexit has put pressure on prices just before Christmas and while normally a high interest rate in recent times has been attractive to trades, in this case it was certainly not. One thing that is not clear is if inflation will continue to keep pressure on the UK economy, as most of it was prescribed to falls in the exchange rate in recent times. However, since the exchange rate has recovered and has moved to be more stable. I believe that inflation will likely taper off, unless we see some disastrous Brexit news in the short term. It's also likely that if inflation does persist, an interest rate hike will certainly be on the cards in the near future.

For the GBPUSD it has been a simple slide back lower and this marks the third straight day of losses after so much enthusiasm for the Brexit deal - which David has seemingly commented on not being law causing feathers to ruffle in Brussels. If we are to see further falls then my eyes would be on the key support levels at 1.3256 and 1.3220 which will be a key area; namely because of the 200 day moving average charging up the charts but also the bullish trend line which is also in place. This key level would build a strong case for the bulls to fight back if there were many left in the market. In the event that we do tick back upwards off some positive news and renewed optimism in the pound, then 1.3393 and 1.3438 are going to be the first major levels of interest to trades on the rise.

Some other positive news has been the Tax bill, with murmurings out of the Senate that revisions have been made and could in theory rush through and get on the president's desk by Christmas. This would be a big surprise if it turned up in the coming week, as expectations are that it would take some time. One clear winner of all of this though has been the S&P500 which continues to climb up the charts and is making new ground.

So far resistance levels are looking like the usual candidates, with psychological levels at 2675 and 2700 likely to be the pausing points at present. Support can also be found around 2652 and 2631, but the bears are very scarce when it comes to pressure on the S&P500 at present - especially with the tax bill in tow. It's easy to say that equity markets could be overvalued, but at the present time the markets seem keen to keep on pushing.

It's been a funny day for the USD as it slipped lower on Tax legislation worries. For the most part it has fallen around two senators who are keen to fix the current child tax credits. In reality this is something republicans are likely to help remedy in order to get this bill over the final hurdles and in front of the president to sign before Christmas. However, for me the big mover - and what might have a much more interesting impact - was of course today's retail sales which lifted sharply to 0.8% m/m (0.3% exp). This is a very strong move just ahead of the December rush season and in return we could expect to see GDP forecasts raised for the 4th quarter going forward. I would be surprised if we didn't see solid earnings this season in the equity markets as well given the huge rises in consumer and business confidence. For now it would seem the Trump effect might be still there after all heading into the new year.

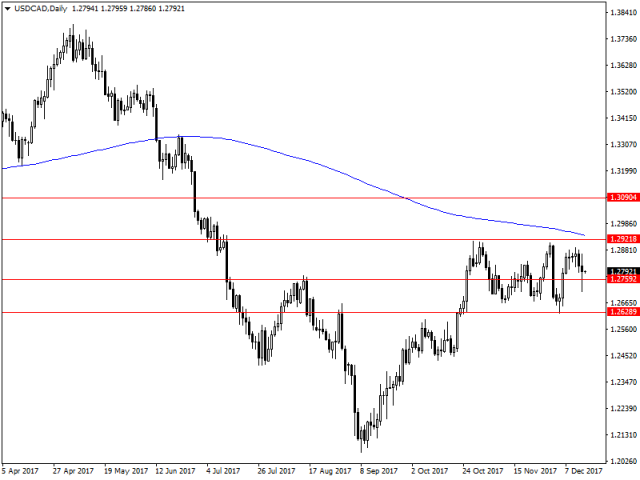

One of the key areas this was felt was on the USDCAD which was swinging heavily today, not only on the USD weakness but also Bank of Canada comments which pushed up the chances of a rate hike for March next year. For the most part the USDCAD has been ranging for some time, and it has struggled to break through the major resistance level at 1.2921, which has so far seemed like an impossibility at present. One of the main reasons also has been the 200 day moving average bearing down on that level which of course adds further pressure. At the same time the swing lower today failed to stay below support at 1.2759 which leads me to believe that the bulls are still in this market despite the Canadian recovery we've seen. If the bulls do leap back into the market 200 day moving average will be the key level to close above, and if we do close above then expectations are that we could see a move upwards to the 1.3000 level. For now though it's a case of waiting to see if the ranging does stop and the trends continue.

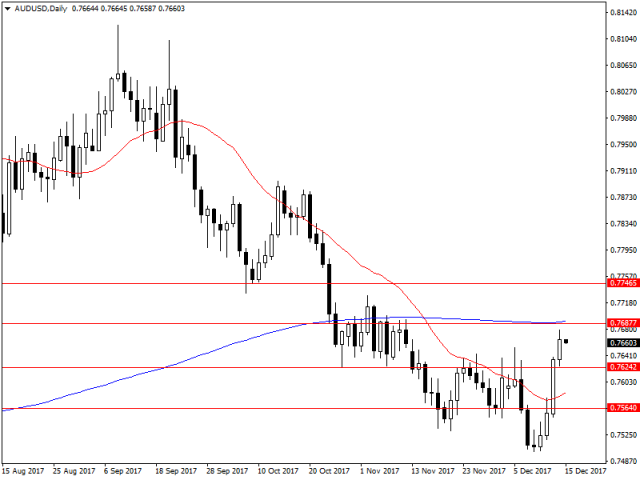

The other key one to watch out for is the AUD, with the market likely to be looking forward now to next week's RBA minutes on the economy and their thoughts after the most recent unemployment figures. We could certainly see the case made for a potential rate rise in the future, but for now it's a case of wait and see - even though the market is fairly bullish.

Chart wise, and it's clear the AUDUSD bulls are back in fashion and looking to make up some ground. After the positive news yesterday and weak USD it is a surprise to see that it has failed to climb higher to the 200 day moving average and resistance at 0.7687. I still believe this is a key level to watch and if we do see further extensions it could lead to bigger things. For now though like the USDCAD it's a case of wait and see as the market looks to enter Friday trading.

Equities reaction muted on tax breakthrough; Watch the bond market

Asian markets woke up on Thursday to the news that Republicans had passed the long-awaited tax bill. President Trump is now just a pen stroke away from overhauling the tax code. Interestingly there aren’t any fireworks on the announcement of Trump’s Christmas gift; because as expected, the good news is already priced in.

In fact, the reaction was more evident in fixed income markets. U.S. 10-year bond yields traded above 2.5% for the first time since March 2017, allowing the yield curve to steepen after flattening for most of 2017. The spread between 2-year and 10-year treasury bonds climbed more than 12 basis points, reaching 63 basis points, after falling to its lowest level in a decade last week. The spike in long-term bond yields is supposed to be positive for the U.S. dollar, as it suggests the Federal Reserve should become more aggressive in tightening policy next year. However, the dollar’s reaction was muted because there’s another side to this story. The additional supply of U.S. bonds due to the unfunded tax cuts, will probably make U.S. treasuries less attractive in the longer run, and given that most central banks are trying to catch up with the Federal Reserve, yields in Europe and other markets are also anticipated to move higher in 2018, thus narrowing the interest rate differentials gap.

The enormous expected increase in U.S. deficit will also put the U.S. sovereign credit rating at risk. If any of the credit agencies- Standard & Poor’s, Moody’s or Fitch downgrades the U.S. sovereign rating, yields will spike even higher. However, the impact on the dollar won’t necessarily be positive, with the opposite reaction being more likely.

The Yen’s reaction was also muted to Bank of Japan’s monetary policy decision. As expected, the central bank kept interest rates unchanged at -0.1% and maintained its 10-year bonds yield target at around 0%. Given that weak inflation is expected to continue dominating the monetary policy outlook, I don’t expect any significant change in policy next year. Thus, the Japanese Yen will continue to take its cue from risk appetite/aversion in equity markets for the foreseeable future.

Euro traders are awaiting the outcome of today’s Catalonia’s election. Polls are suggesting that it will be a tight race between the Catalan Republican Left party, which supports independence and Ciudadanos which is in favor of a unified Spain. Given that the election is not expected to be decisive and parties may form coalitions to govern, the risk of tensions flaring with Madrid again, remain limited.

With only two trading sessions remaining for 2017, liquidity dried up across the global markets. This has been obvious in U.S. and European equities, where volumes dropped significantly. However, some investors continued to tweak their portfolios slightly, leading to insignificant price action. I don’t expect equities to deviate much throughout Thursday and Friday.

Interestingly though, traders continued selling off the U.S. dollar. One could blame Wednesday’s U.S. consumer confidence report which fell from a 17-year high, but the dollar was declining before the release. I think the best explanation for the dollar weakness is the sharp fall in U.S. Treasury yields.

10-year bond yields dropped 7 basis points on Wednesday, to reverse almost 50% of the gains from mid-December towards last week, where yields broke above 2.5% for the first time since March 2017.

Despite appetite for risk sending Asian equities to record highs on Thursday, the safe haven Yen is outperforming its major currency peers. USDJPY dipped below 113 for the first time in six trading days after the release of Bank of Japan meeting minutes. Some members are considering tightening monetary policy, if the economy continues to improve next year. This would be a significant shift in strategy for a Central Bank thought to be the last to exit the unconventional stimulus packages. However, I don’t think the BoJ will move anytime soon due to subdued inflation; but, given the lack of liquidity, moves in currency markets may be exaggerated.

Commodity currencies are also enjoying a decent upside, after copper prices rallied to their highest level in almost four years.Oil prices remained close to a two and a half year high, and gold hit a one- month high. Considering that no Tier One economic reports will be released, the Aussie, Kiwi, and Loonie will continue to follow commodity prices direction.

Daily Fundamental ForexTime ( FXTM )

FOMC minutes give some life back to dollar bulls

The latest FOMC minutes have given the bulls something to be happy about, as the FED once again looked to keep the pace of rate hikes in the near future. There were some key takeaways from the meeting and the most pressing was that FED officials expect inflation to rise to 2% in the medium term as the Tax bill has a impact on the US economy. Expectations were also strong that pressure on the labour market as unemployment further drops would also help boost inflation expectations, and that potentially forecasting of inflation may also have been low historically. So with the FED looking forward in 2018 and Trumps man Powell about to come to the table we could potentially see some strong bullish moves from the FED with a strong US economy in front of them.

For the USD bulls it was positive across the board with large rises against all the major pairs, but mainly the European ones. For me one of the more interesting ones continues to be the USDCAD which lifted slightly, but is still lacking the momentum required to break out of the current bearish trend it finds itself in. So far traders will be watching to see if there is a bounce at support at 1.2427 to see if the bulls can come back into the market, otherwise they could be waiting until 1.2108 to see any sign of a solid bounce. If we see a push back higher 1.2628 and 1.2759 are likely to be the first key levels of resistance. However, the 200 day moving average is creeping down and likely to also act as dynamic resistance in the current market climate.

For me the main thing that keeps on going in the bullish American climate is the equity markets at present, and look no further than the S&P 500. It's getting hard to believe that there is an end, but at some point the bears will look to swipe. For now though, the Trump effect and the recent Tax reform coupled with a FED with positive forecasts is driving American companies higher than ever before and in the process lifting the S&P 500 higher than ever before. Most weeks we are seeing a new record high at present, but that being said uncertainty could be the instability that shakes the bulls off the top for a bit.

On the charts, and as previously stated, the focus would ideally be on psychological levels - as the market continues to rise it will look for these points. I would anticipate that markets will continue to look for key levels at 2725 and 2750 if the bulls look to push higher. Any swings lower are likely to get held up at 2700 as it acts as support in the current market. However, a push through would be treated with concern as generally speaking the 2600 and 2500 level were previously very good at holding back the bears.

A critical week for the US Dollar after a fragile start

After having the worst annual performance since 2003, the dollar continued to struggle in the first trading week of 2018. The dollar index fell to a three-and-a-half-month low to trade below 92, leaving many traders wondering whether this year will be another devastating one for the greenback. When looking at the Commitment of Traders (COT) report, speculators are not showing interest in buying the U.S. dollar yet, and the latest bunch of data did nothing to support the dollar.

Friday's jobs report did not motivate the dollar bulls to return, with non-farm payrolls rising 148,000 in December versus expectations of 190,000. Although I think the numbers weren’t bad and the labor market remains healthy with unemployment at 4.1%, wages are not yet showing signs of accelerating, and this remains the key missing ingredient of the U.S. economy’s recovery.

The latest minutes of the Fed’s meeting also showed that policymakers aren’t sure whether inflation will return to the central bank’s target which is why markets believe that only two rate hikes will occur in 2018, as opposed to the three in the Fed’s dot plot. This week many Fed speakers are due to speak including the two dissenters against a rate hike in December, Neel Kaskhari and Charles Evans. Whether they have changed their mind, or still believe rates shouldn’t be hiked, remains to be seen but we’ll also tune into other Fed speakers for fresh insights.

If the Fed speakers don’t deliver news, tier one economic releases may provide the needed clues. Consumer prices and retail sales are both due for release on Friday. Given that energy prices spiked in December consumer prices are expected to increase 0.2%. However, I think traders will be more interested in the core CPI figure, which strips out volatile items like food and energy. Any upside surprise in the inflation numbers will likely bring back the dollar bulls.

Given that the major U.S. economic releases are four days away, many traders will focus on whether any technical breakouts will occur. EURUSD failed to break above 1.2092 (2017 high) last week, but a successful breakout will likely lead to further buying of the single currency towards 1.22. Similarly, Sterling is only 100 pips short of 1.3656 (2017 High). So traders should keep a close eye on these levels.

New Video from #FXTM#MarketUpdate with Research Analyst ForexTime, Lukman Otunuga

Global equity bulls were in the vicinity during Tuesday’s trading session as world stocks remained at elevated levels. In the currency arena, the Dollar appreciated amid optimism over higher US interest rates. With the economic calendar relatively light today, price action may dictate where currency and commodities trade.

- The #EURUSD is pressured below 1.20 on the daily charts

- #GBPUSD bears are eying 1.3520

- #Gold remains bullish above $1300

The US markets have continued their hectic pace this year as the S&P 500 reached new highs on the back of economic figures. These figures showed that while initial jobless claims lifted to 261K (245K exp), the continuing claims figured dropped to 1.87M (1.92M exp) which shows that Americans are certainly getting back into the work force. Tomorrow though will be a big day for the US economy as retail sales data is due out. This a big deal when you consider the fact that the US economy is very much a consumer based economy and big swings here can have large impacts for the global economy. In addition to this, we are expecting to see some CPI data which will also weight on the FED in regards to rate hikes in the coming year. It's quite exciting to have such a serious amount of data at the same time, but I would expect large swings as a result of the volatility.

For the S&P 500 traders it is still tracking to make 2800 by the end of next week at its current progress, which seems unreal, but that is the bull market we seem to be in. At present the S&P 500 is actually hitting a new high every 48 hours as well. For me though the S&P 500 is still a threat to some bulls as the market is looking to take a swipe and have a correction at some point in the current market climate, it just has not found the opportunity. Resistance levels can still be found at the psychological levels of 2775 and of course 2800, with 2800 likely to be a tough level to crack through if 2700 is anything to go by. If we see the bears in the market then I would anticipate support at 2750 and of course 2725, but at the same time we've seen no real bearish action since November.

I touched yesterday on the oil markets and yesterdays news on another strong drawdown is likely to be a positive signal for the oil bulls. OPEC members will continue to see the benefits of holding out on production cuts and are likely to continue them. I feel that for some time now we could see oil to continue to rally until it touches the 100 dollar a barrel mark, where the market starts to kick in and it seems unreal.

For Oil traders the levels still remain the same with 65.94 and 69.49 as the major resistance levels in the current market, based off previous strong levels. There is also the question of support in this market and it can be found at 62.12 and 59.08, but there is a trend line in the market that people should be aware of as lately it has been respected by traders on both sides of the coin. The question is how much longer is it here to stay.