Sterling slides, Bitcoin tumbles & Investors seeking more clarity on tax reforms

Sterling fell more than 0.5% early Monday, after the Sunday Times reported yesterday that 40 Conservative Party MP’s agreed to sign a letter of no confidence in the Prime Minister, Theresa May. While this remains short of the 48 votes needed to force a new leadership, it still creates much frustration amongst investors seeking clarity on Brexit negotiations. With May’s position being potentially at risk and no significant progress after six rounds of talks with EU, Sterling may come under increased pressure in the next couple of days, with the 1.3024 support level at risk of being breached. A leaked letter from Boris Johnson and Michael Gove pushing for Hard Brexit, add to the uncertainty as House of Commons meet on Tuesday.

It is also a busy week on the UK’s economic data front, with Consumer Price Index, Producer Price Index, labour data and retails sales due to release. However, politics are likely to remain the dominant factor moving the pound this week.

For investors finding the low volatility environment boring, have a look at Bitcoin. The cryptocurrency lost more than quarter of its value after reaching a high of $7,888 on Nov 8. The cancellation of a plan to increase the bitcoin’s block size “Segwit2x” on Wednesday, is what to be blamed for the price crash, but given that prices rallied $400 on Monday it seems the news has been digested. We have seen similar steep falls in Bitcoin throughout the year; specifically in June and September, but every time a considerable decline occurs, new investors jump in to experience the new asset class. The increasing investor interest in the cryptocurrency market has pushed CME Group to announce the launch of a bitcoin derivative soon, indicating that more fund managers and professional investors will become involved. Although Bitcoin might not be a suitable asset for conservative investors due to its volatility, I still see a great potential ahead.

Given that the earnings season has come to an end, equity investors will shift their attention to the U.S. tax reform plans. There is a considerable difference between the Senate and the House on how to proceed, and if no clear path evolves, I expect a further pullback in equities. The Senate’s proposed delay of the tax cut until 2019 is definitely not what President Trump is looking for, so it remains to be seen whether he can push Republicans to unify when he returns from his Asia tour.

It should be all good news for global equity markets at present as the global recovery continues to tick along nicely. So far profits are up and the market has been bullish, especially around developed labour markets. However, have we overextended at present? If you've been watching some of the major indexes you might very well think that. Recent trends in global markets have so far been bearish which is a surprise, but when you consider the level of uncertainty and the fact that rates are on the move higher it does make for some interesting thoughts and trading ideas. So far yields are looking like they're increasing in the long run, which bodes well for investors looking to move out of equities.

The S&P 500 has come up short of the magical 2600 mark at present, this despite the recent news off the wire about NAFTA renegotiations being positive. PPI was also positive today, but once again markets were not having a bar of it, and looked to sell off. So far the S&P 500 has held up on support around 2580 where it has managed to sit above over the last few days, the 20 day moving average is also providing some additional support. Further movements lower are likely to hit key levels of support at 2565 and 2545. Just looking at the daily movements, it's very hard to say if this is the time for a correction. Certainly, markets are feeling like one is overdue, and historically data says that is the case. The question here is when and how bad, but for now the bulls have the trend and market corrections are rare for the S&P 500.

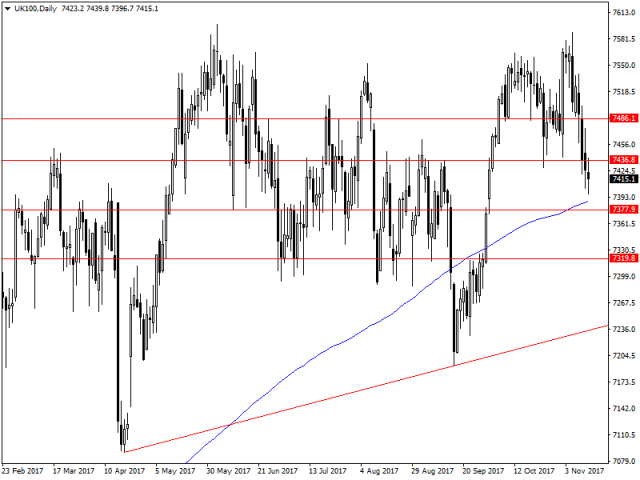

A quick glance across the Atlantic at the UK equity market and it's a similar story, just this time the market is being dominated by politics and of course the Brexit debacle. Mark Carney must have been breathing a sigh of relief today as CPI was not as strong as the previous month at 3% y/y, thus taking the pressure of the needs for any further rate rises at this time. Markets, however, were not so interested as the FTSE 100 dropped on the news and continued to be weighed down by global sentiment around equity markets.

FTSE 100 traders will be looking to extend the trend lower if with the bears, but so far we've seen weaker and weaker candles which is a sign of caution from them. There is the possibility of the bulls swinging back into the market here and potentially pushing for resistance at 7436 and 7486 on the charts. If the bears do extend lower than the 200 day moving average, it will be key to watch here to see if traders respect it. With weaker candles that could be very much the case. Support levels below this can be found at 7377 and 7319 for the bears.

It's been a positive day for US economic data as retail sales surprised analysts lifting to 0.2% (0.0% exp). This shows a strong build up in the period before Christmas where retail sales is generally quite strong as well, and will bode well for the economy and the FED which is a big follower of the consumption based economy that is the USA. Further adding to fuel to the fire was of course CPI data which I touched on yesterday with Core CPI y/y coming in at 1.8% (1.7%) exp. While not the magic 2% mark the FED does chase it was certainly a positive reading and shows that the economy is turning over nicely in America. The real question will now be if fiscal policy from the Trump administration and can translate into real gains for the economy, or if his legislation will continue to struggle through the house and senate in America. It would be a strong mover of the dollar is something was passed with tangible gains in the near future, but so far the market is in wait and see mode on the fiscal front.

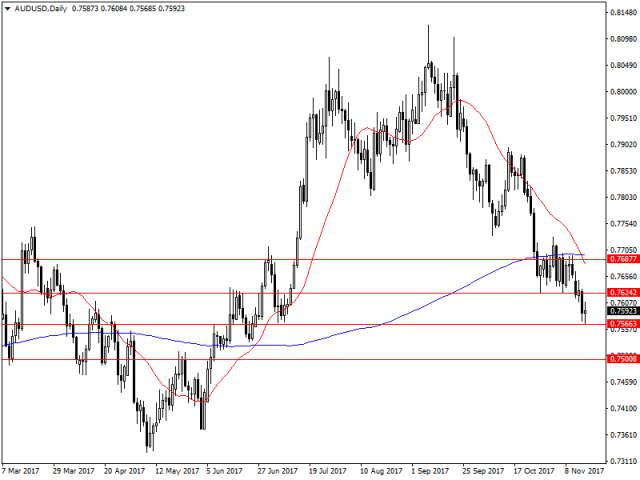

One of the major losers as a result of the USD boost was of course the Australian dollar which has lost ground after last night's economic data which showed wage growth being underwhelming. With the wage index coming in at 2% y/y (2.2% exp), showcasing that while the job market is strong wage growth is not following it and inflation will cause issues in the long run for the Australian economy if wage growth does not catch up. With the AUD now pushed against a wall traders have been of course waiting on the employment figures due out. Of course they've not been the best with employment dropping sharply to a reading of 3.7k+ (18.8k+ exp), but the unemployment rate falling to 5.4% accordingly adding some consolation for AUD bulls at present.

On the charts the AUDUSD has not been this low since July and markets will be looking to see support at 0.7566 on the charts or if it will struggle to extend any lower and we see the predictable bounce in the AUDUSD. As the employment data is bad markets have overreacted and driven the AUD lower to support at 0.7566 where it has looked to take a breather at this key level. If the bulls do come back into the market - and it's really a maybe - then resistance levels can be found at 0.7624 and 0.7687 with the respective movements if things became worse from a fiscal point of view. Reality is however, that the bears are likely to have another crack and potentially force it down to the 0.7500 key level at present with the potential to fall further at this present time.

The Tax bill has been talked about for some time, and today was the day for it. Obviously, it cleared the US house easily enough and is now on its way to the senate; where the republicans have control as well. What does this mean for markets? Well put simply it cuts corporation tax from the current 35% to 20% - a very large jump - which means US companies are likely to record larger profits which of course will have a flow on effect for the economy. The real question here is if the republicans in the senate will be able to push it straight through or will look to make amendments. They are after all different creatures in the senate and the tend to be more heavy handed when it comes to clearing large bills like this through government. However, with a two seat advantage it looks like it may just shine through and Trump will be able to sign it all off before Christmas - giving him his first major win of his presidency.

For equity markets the rally has been pretty sharp as a result of the tax bill. Traders are betting that in the long run this tax bill will unleash the corporate machine that is America and record profits will accordingly flow through. The S&P 500 today was a prime candidate for this as a I previously noted, and accordingly has rallied sharply. Resistance at 2580 was no match for traders looking to enjoy the rally today and now it's a case of targeting 2600 for many bulls in the market. If the senate does indeed push the bill through then 2600 may be a support level as the market will jump sharply I feel - given it's the last hurdle. With a tax reform like this the possibility of even pushing the 3000 mark becomes all the more realistic. If we see the bill struggle then we could see sharp drops on the charts to support levels at 2565 and 2545, with the potential to go further as it feels a lot is riding on this bill in the equity markets.

The Australian dollar was one I also touched on yesterday and while the unemployment rate fell to 5.4% (5.5% exp) the participation rate was lower, and accordingly the creation of new jobs only came in at 3K so it was disappointing for traders in reality. I still feel that the AUD will struggle in the long run given the pressure on the economy, and as the USD continues to find favour with traders again.

The AUDUSD on the charts currently has been trading between resistance at 0.7462 and support at 0.7566, with market expectations of potential falls lower. The 0.7500 psychological level is currently likely to be the largest target if the trend continues. However, we could see a bounce here and a retest of resistance levels at 0.7624 and 0.7687 on the charts.

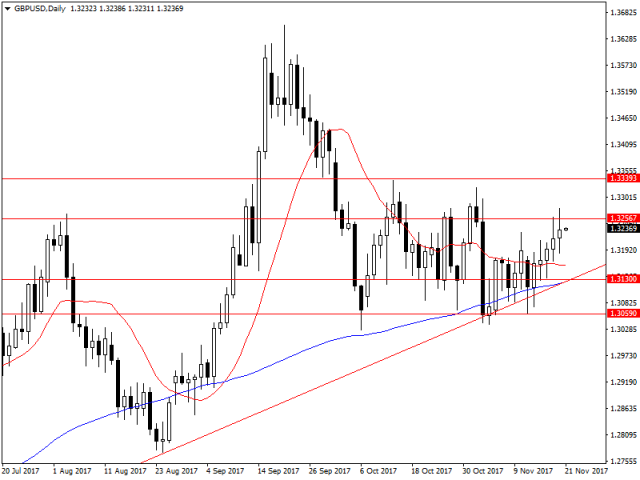

The Euro had a pause for concern in the evening trading session as the coalition talks in Germany fell apart leading to a political crisis in Germany. This now presents the toughest challenge Angela Merkel has felt in over 12 years of being at the top, however, she seems somewhat composed and is keen to send the parties back to the polls in order to get a majority government. So far though polls have predicted that anti immigrant parties are likely to gain more momentum than the traditional centrist parties which have dominated German politics in recent decades. And for Brexit this will certainly put pressure on the British government now that Merkel is currently off dealing with her political crisis, rather than being focused on there's. For some time many had expected her to get involved and sort out the crisis, but that's certainly not going to be the case and £40 billion bill the UK is offering to settle the bill is being put to the table.

The British governments ability to settle the bills is likely to be a game of brinkmanship and the EU does not have to blink at all. What could well be worth their time is to let it play out internally as right now a number of backbencher Tories are upset over the size of the number and could in theory force a leadership vote. While plausible I do believe that the government is likely to try and push it all through as rapidly as possible in order to get backing from business. Either way the pound is likely to encounter some rough waters over the course of this week as a result.

On the charts the GBPUSD continues to be inching its way higher on the charts, and thus far it's been on the back of some USD weakness which has been apparent. However, the recent moves higher have shown an abrupt weakness in bullish potential and we could see bears come back into the market to tighten things up before breaking out. Resistance levels for the GBPUSD can be found at 1.3256 and 1.3339, but the band in between this is likely to see a lot of action. In the event that markets turned south they would have a tough time battling the 100 day moving average which has been acting as dynamic support, and also support levels at 1.3130 and 1.3059. A breakthrough of these support levels could send the pound tumbling though.

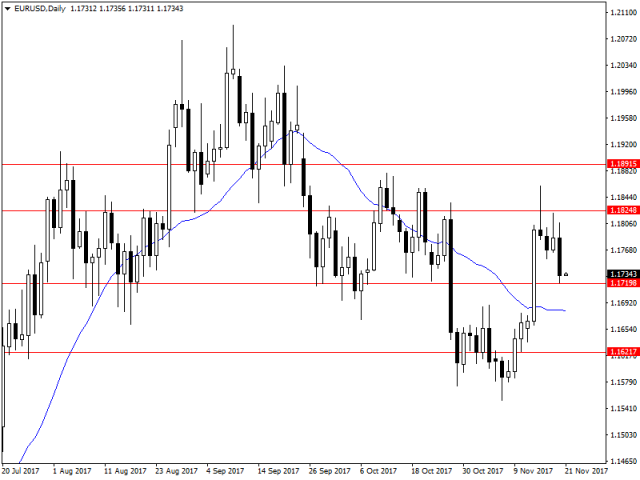

The EURUSD is also looking weaker after the political news out today, and for me the focus will be playing of the political news out of Germany going forward. Key resistance levels can be found at 1.1824 and 1.1891. Support levels can also be found at 1.1719 and 1.1621, with the trend looking all the more bearish as of late. Certainly also for the euro the USD weakness will be a primary factor, but so far it' s a mixed bag.

Global stocks rally, Sterling on standby ahead of UK budget

The healthy combination of rising corporate profits, strong global growth and cautious optimism over U.S. corporate tax cuts, simply reinvigorated global equity bulls on Tuesday – boosting stocks across the globe.

Asian shares headed for a record close during early trading on Wednesday, following Wall Street’s robust gains overnight. European markets concluded mostly higher on Tuesday and may open on a positive note today as market players continue to shrug off the political uncertainty in Europe. With U.S. stock indexes marching to record highs yesterday as technology and health stocks rallied, it will be interesting to see if the upside momentum is maintained this afternoon.

Chancellor Philip Hammond in the spotlight

Chancellor Philip Hammond will be in the limelight today as he presents the U.K. budget statement to the House of Commons. While Hammond’s speech may revolve around managing the housing crisis, investors will be paying attention to the Office for Budget Responsibility (OBR) which is expected to trim Britain’s GDP growth forecasts. If the overall tone of the budget statement is gloomy and Brexit concerns making an appearance, Sterling is likely to find itself under renewed selling pressure.

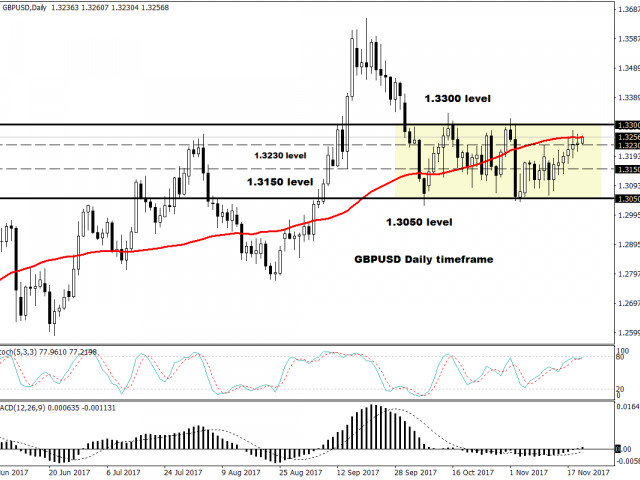

Taking a look at the technical outlook, the GBPUSD has found light support at 1.3230. An intraday breakout above 1.3250 could encourage a further incline towards 1.3300. Alternatively, a failure for prices to keep above 1.3230 may encourage a decline to 1.3150.

Dollar lower ahead of FOMC minutes

The Greenback weakened against a basket of currencies on Tuesday, after Yellen’s cautious remarks reinforced market expectations of the Federal Reserve raising interest rates at a gradual pace.

Yellen cautioned that raising interest rates too quickly could obstruct the Feds efforts to reach the golden 2% target and reiterated the fact that this year’s low U.S. inflation remained a mystery. With the outgoing Fed chair uncertain over the stubbornly low inflation being transitory, investors were left pondering over how this could influence the central bank’s monetary policy strategy in 2018.

Much attention will be directed towards the minutes from the latest FOMC meeting this evening which should offer further clues on the central bank’s outlook future interest rate increases. With markets widely expecting U.S. interest rates to be increased in December, investors are likely to closely scrutinize the minutes for fresh insight into monetary policy beyond 2017.

The Dollar could receive a boost if the minutes are presented with a hawkish touch, alternatively, if the minutes express concerns over low inflation and fail to bring anything new to the table, sellers may make a move. From a technical standpoint, the Dollar Index is coming under pressure on the daily charts with resistance found at 94.00. Sustained weakness below this level may encourage a further decline towards 93.50. Alternatively, a breach back above 94.15 puts this current bearish setup at risk, with the next level of interest at 94.50.

FOMC meeting minutes are always greeted warmly by the markets, as a glimpse of the potential future direction of the FED going forward, and today didn't disappoint at all. As predicted the FED was positive about the possibility of a December rate hike before the year goes out, and the market has aptly priced this in. Markets on the other hand were caught off by certain members reluctance to actually lift rates as they felt inflation was starting to slow down and the previous large rises may not continue going forward. Now with Yellen set to resign and the new head of the FED taking over, it may be the case that we do see more hawkish movements. But the board is a democratic vote, so unless we see real movement there it becomes very unlikely at this stage and the doves could be staying on for some time.

For traders the USD sell off in safe-haven currencies was strong with the USD losing a number of points especially against the Yen. USDJPY was by far the most volatile trade of today, which surprised many given how flat it had recently been, but markets were quick to punish the FED over its dovish comments. One of the major reasons behind the sudden appreciation of the Yen is that thus far Abenomics has not been as active as expected and it continues to be at a risk of being devalued quickly. It's also a fantastic storage for traders looking for some sort of safety within the markets and a traditional one at that as well. However, for the USDJPY bears the time to jump was today and they certainly did.

USDJPY bears crashed through the 200 day moving average ruthlessly as they looked to push the pairs to strong support levels. Support at 111.133 was able to holt the downward trend, but so far is the only thing holding back the USDJPY from storming any lower. Markets looking to swing lower further are likely to find another strong level of support at 110.202, but the market may take some breather here and give up some gains. For traders looking for a bounce higher then resistance can be found at 111.944 and 112.787. The reality for the bulls jumping back in though is slim, as this bearish trend is likely to push traders back in the water in search of blood.

After the recent failures of traders to break through resistance at 114.359 over the previous month, it's no surprise that the market has jumped on a bearish trend. The question is though will it continue to run, or will markets look to pause and take stock of the volatility we've seen today. My thoughts are that it could potentially slow down but still trend, which would be promising for traders looking for an easy wave.

Stocks drop, currencies range bound & bitcoin eyes $10,000

Most Asian indices edged lower on Tuesday, following a mixed session on Wall Street yesterday. China is becoming a key market to watch, as it’s leading the direction for other markets across Asia. Rising bond yields are threatening corporate profit margins for the second largest economy; meanwhile Chinese authorities are helping to drag equities lower, after sending alarming messages about a potential bubble being created in large-cap firms. Given that China continues to focus on quality rather than quantity growth, it’s not surprising to witness action of this nature from the Chinese government in an attempt to mitigate bubbles in asset prices. However, such actions may have a negative impact on sentiments that could spread across other Asian markets.

U.S. equity traders are in a wait-and-see mode. President Trump will meet senators today at their weekly policy lunch, to ensure that Republicans are on the same page regarding the tax system overhaul. I firmly believe that U.S. legislative tax reforms are strongly “priced in” the U.S. markets, thus if significant tax reforms do not pass, I expect a substantial decline in major indices, particularly in small caps. Given that the effective tax rate currently stands at around 27%, taxes should be brought below 25% to be effective. Republican Senator Ron Johnson said he would vote against the bill unless his concerns about the legislation are resolved. Given that other Republican Senators share Johnson worries on deficit implications, passing the bill does not seem to be a done deal yet.

Currency markets were trading in narrow ranges early Tuesday, as investors brace for UK bank stress test results, BoE’s Carney Speech and the Fed speech, including Powell’s Congressional address. On the data front, the U.S. Goods Trade Balance, and the Housing Price Index are likely to have minimal impact on the USD.

At the time of writing, Bitcoin scored a new record high of $9,886 in an attempt to break above the critical $10,000 threshold. Bitcoin has become a very hot topic and many fund managers have raised the price target for the cryptocurrency. Yesterday, former Fortress hedge fund manager Michael Novogratz commented on CNBC, that bitcoin could be at $40,000 by the end of 2018 and he expects that total market capitalization could reach $2 trillion, from $309 billion currently. I think that we will hear more skyrocket predictions, but few will provide an economic metric that supports their valuations. It will be interesting to see how the market reacts when Bitcoin breaks above $10,000.

It's been a crazy day on the markets and the GBPUSD has been a clear winner when it comes to movements today as the Market has reacted positively to the so called 'Divorce Bill' from the EU that Britain is meant to pay. So far people are expectong the figure to come in around 50-60 billion pounds that would be paid out over 40 years. Obviously, this is a large number for any sovereign nation, but it enables Britain to plow forth in its so called negotiations. The market is now looking for the next steps for the UK economy, as it expect to see some sort of trade negotiations come out of all of this. I do think that it might be a bit of a while off that we do see something realistic, the fact being that a) the UK has no strong leg to stand on, and b) it's always a long road to what people expect will be a result. Either way the volatility in the GBPUSD is likely to continue into the near future especially with the current pace of news and politics involved in Brexit.

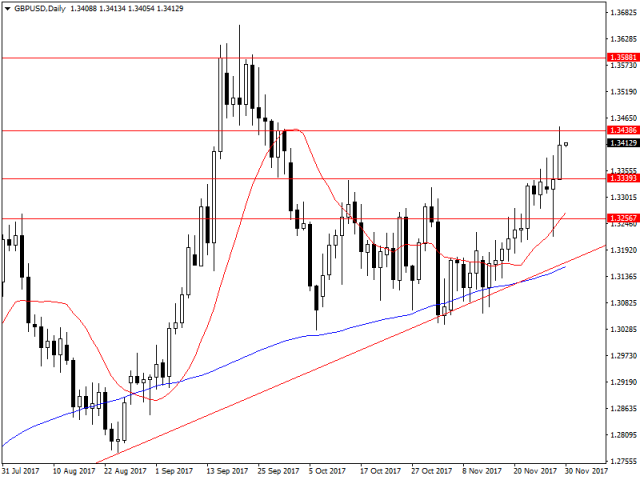

On the charts it's clear to see that the bulls are back into the market and are climbing higher. Yesterday we were talking about the 1.33 levels, and today we are in the 1.34 levels which shows the market is keen on these talks. After touching resistance at 1.3438 the market has pulled back to take a breather, but the real key level is to be found at 1.3588 which is where bullish traders will be looking to aim in this market. In the even the bears do regain control and look to push it lower then support at 1.3339 is likely to be a prime candidate for support as well as 1.3256. Traders should also be aware of the previous trend line which continues to be an obstacle for any bears in the current market.

The US also continued its stellar run today with US pending home sales m/m lifting by 3.5% (1% exp) once again showcasing the strength in the USD. On top of the traders were also somewhat bullish about the first round of the senate tax review of the Trump tax bill, which is likely to boost the US economy - even though running a deficit for a bit. One of the big losers for this has been the commodity currencies which have been bearish against the USD with all this support.

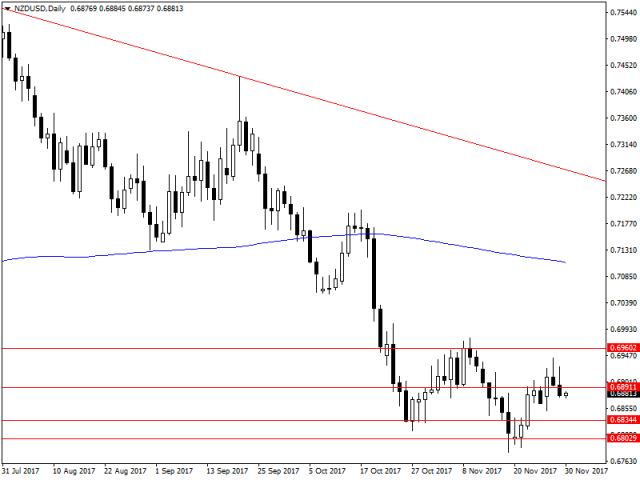

For me the NZDUSD continues to be one of those currencies that will struggle with a resurgent USD in the current market climate. So far all the candles have shown exhaustion by bulls in the market as the NZDUSD dipped under resistance at 0.6891. The market is now looking to extend further lower to 0.6834 and 0.6802 on the charts, as the market looks to push it back into the red. For me the bulls are going to be a real threat until the USD gives up some ground as the NZ economy is still struggling in the interim while it figures out a new government.

With a US tax bill and a Brexit currently flying around in the markets it's hard not to get lost on the bigger picture for other countries as well. However, the Bank of Canada (BoC) is one that we should all be paying attention to as in the next 24 hours they will have their monthly interest rate decision, as well as follow up conference to the market. Now a interest rate is not priced in at present - in fact the odds are very low, but the BoC has a habit of surprising markets and the recent employment figures were very positive adding further weight to the potential for a rise. I don't anticipate we will see a surprise interest rate jump, however the words that will be used will be vital for the market when it comes to pricing in the next interest rate rise and of course are likely to have a big impact on the Canadian dollar. It's not always about oil for the Canadian economy, but one thing is clear there is certainly more to offer on the trading calendar than oil updates.

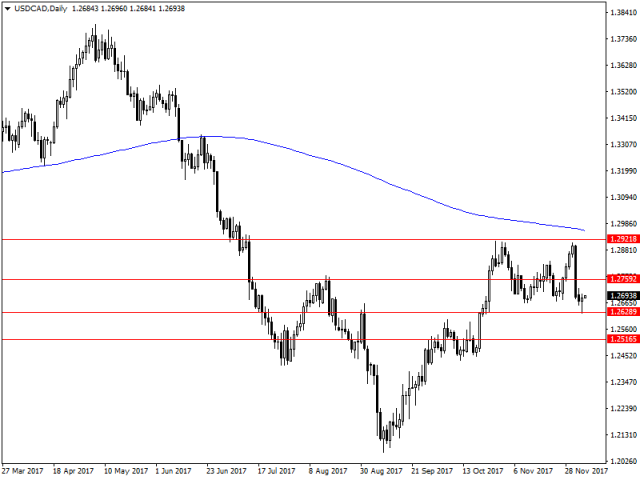

So far the USDCAD has been a big mover and has held up nicely on the charts in preparation for the upcoming announcement. So far the USD has been losing ground against the CAD after traders were quick to attack on USD weakness and the strong jobs report. Any movements higher on the USDCAD were likely to struggle regardless with resistance at 1.2759 and 1.2921, but also with the 200 day moving average starting to ebb lower and showing a pattern of being respected strongly by the USDCAD. Movements lower are likely to find support at 1.2628 and 1.2516 in the current market, but I would also watch out for the oil figures as well, as a strong drawdown would put further bearish pressure on the USDCAD.

One of the key metal markets which has been moving sharply lower recently has been silver which has been reacting sharply to the boost in equities. There has been talk recently that metals could potentially be replaced by Bitcoin and the likes, but I don't believe they represent a tangible hedge like precious metals do in the current environment. What is clear that the US economy booming is starting to have a negative effect on the price of silver and the market is starting to shift lower as a response.

I've always been a fan of silver and the trend is looking quite strong on the charts so far for the bears. Support has held up nicely at 15.996, with the potential to move event further lower to 15.556. Resistance is currently high in 16 dollar region at 16.546 and 16.863 at this stage. All in all though the bearish trend is strong and could continue in the current environment if we don't see any large hiccups.