The pound has been the strongest currency today on the back of positive Brexit news that the UK government is looking like it may have it under control. The Prime Minister of the UK, Theresa May spoke positively to the house of commons today about talks in private with the EU and that they were much better than what the public realised. She was quick to show strength around negotiating the exit from the EU and also retaining access to the single market. It will be interesting to see what the EU has to say on this however, as they've said it will take a miracle to get all of this over the line. Especially with the major point of freedom of movement being the elephant in the room that seems to cause Brexit to trip up constantly. Further news will certainly develop during the course of the week, but I can't see the EU backing down and being positive around talks anytime soon, especially as they seem to have a lot of leverage in this negotiation.

Looking at the charts and it's clear to see the GBPUSD bounced sharply on the 100 day moving average, showing that there is very much the case for bulls to stay in this market. With the prospect of a Bank of England rate rise in the near future there are positive signs for the pound, but that won't be an event till next month. Resistance levels higher are looking like key targets at 1.3219 and 1.3339 at this stage, and I would expect the potential for further extensions higher as well if the BoE talks about the rate rise prospects more so. If the market does slip lower I would watch the 100 day moving average and also the bullish trend line which has been in play for some time. This is a key area for the bulls to take advantage, when looking to tackle the bears.

The Euro has also been an interesting one as well as the EURGBP continues to be a bit of a battle between the two Brexit sides, and it certainly has clawed back a lot of ground over the past year of all this turmoil. After dropping sharply the Euro has managed to grab back some ground from the Pound but it looks unlikely to continue unless the UK can make real promise on its Brexit talk.

At present the EURGBP came under selling pressure today, but support at 0.8918 showed that many traders still believe the Euro is going to be the winner in the long run. The 100 day moving average also added to the bulls favour as well with the support level. Expectations are that if the Euro-zone shows a strong hand then it could lift higher to 0.9038 and further levels at 0.9136. I would expect that it could potentially go higher, but we could see some back and forth in the mean time so it's hard to say just yet.

The Euro has rallied in later trading after waiting on to hear the speech from Puigdemont in the Catalan parliament in Spain. There had been concern from Euro-zone members that Puigdemont the president of the Catalan province may use the speech to declare independence from Spain which would have cause some major issues. However, he never went on to declare independence, but instead suspended the idea under the guise of further talks with Madrid. In all reality this is likely to end badly for Puigdemont in the long run as Spain is now holding a special cabinet meeting on Wednesday in order to deal with the issue. What is certainly clear though is that no EU leaders support such a move and after today's speech the Euro has rallied sharply on the belief that nothing more will come of this in the long run which could disrupt the Euro-zone project.

For the EURUSD traders tomorrow I expect they will be expecting a very strong response from Spain and I would expect the bulls to take full advantage of the situation to push the Euro higher. The EURUSD failed today to gain further ground, after touching resistance around 1.1814, as it waits on the Spanish government response. Further potential extensions are likely to target key levels at 1.1915 and 1.2000 in the long run. If the Spanish government is seen to be weak then I would expect support levels at 1.1719 and 1.1621 to come back into the fray, as the bears look to capitalise on the weakness. It's also worth paying attention to the 20 day moving average, but I expect that the market will be focused on fundamentals instead of technical's tomorrow given all that is happening in Spain.

Across the world in New Zealand and the major political parties are currently going through negotiations with minor political parties in order to form a government after the most recent election. It's a case of demands from the minor parties as they hold the balance of power, and the uncertainty (much like Spain) has been weighing on the currency in the face of an active market. You only have to look at the AUDUSD which normally is a close mirror to the NZDUSD to see the deviation caused by political instability. So far the market is wondering which side the minor parties will go with, so much so that the NZD has not moved but this Thursday is meant to be an indicator of how things will go.

For the NZDUSD traders, the focus is on support at 0.7054 which is currently holding up further drops. The expectation is that a left-wing leading party gets into power then we could see further NZDUSD drops into the 60 cent range. With support levels at 0.6983 and 0.6921 likely to come under pressure. If we see a right-wing party come into power (which was the previous government) then the market will likely jump and put pressure on resistance levels at 0.7166 and 0.7219 respectively.

When the Federal Reserve met on 19-20 September, it announced the start of winding down the $4.5billion balance sheet and maintained plans for a third-rate hike in 2017. The statement reflected confidence in the economic activity particularly the pickup in household spending and growth in business investments. Despite the storms Harvey and Irma, the central bank was still confident the U.S. economy would keep its momentum, and Janet Yellen sounded more hawkish than markets anticipated. This was all good news for the U.S. dollar which rallied for three weeks after the meeting, appreciating 2.3% against a basket of currencies.

The primary concern was low inflation. Fed chair Janet Yellen described it as something of a "mystery." When an institute which employs over 300 Ph.D. economists still doesn’t know whether low inflation is persistent or transitory, the risk of tightening monetary policy further might be a huge policy mistake if inflation did not return to normal levels. The Phillips Curve Model which theorizes that there should be a strong inverse relationship between unemployment and price inflation is apparently not working, and probably it is time for the Fed to drop this theory and find new models.

Yesterday’s Fed minutes reflected such worries. Several members insisted that the decision of raising rates for the third time in 2017 should depend on economic data which increase their confidence that inflation would move towards the Fed’s 2% inflation target. The dollar bulls did not like the statement despite expectations of a December rate hike remained above 80% according to CME’s Fedwatch Tool. The dollar index continued to fall on Thursday for the fifth day in a row, with overall declines of 1.5% from Oct-6 highs.

Given that inflation has become the most important economic metric impacting the dollar’s direction, today’s PPI and more importantly tomorrow’s CPI should be watched very closely. Any upside surprise would curb the dollar’s fall; however, a disappointing figure would be an excuse to keep dragging the USD lower.

The Euro performed very well, climbing to the highest level in more than two weeks at 1.1878. After Carles Puigdemont suspended the process of Catalonia's independence, Spain’s Prime Minister Mariano Rajoy has given him five days to say whether or not he has declared independence. Depending on the response, the government in Madrid could impose direct rule on Catalonia. I think the overall crisis in Spain is still underpriced, and if no agreement is reached in the next couple of days the stability of the Eurozone as a whole would be at risk. Although economic fundamentals continue to support a stronger Euro, politics will play a significant role as to where the Euro heads next. ECB’s Mario Draghi will participate today in the annual meetings of the World Bank Group and the IMF in Washington. Any new hint provided will move the single currency.

Despite no advances made in the Brexit negotiations, Sterling continued to trade higher against the dollar for the fourth consecutive day. Although Brexit will keep weighing on Sterling on the longer run, monetary policies seem to be the major driver for now. Expectations of BoE raising rates in the final quarter of 2017 remained high, thus narrowing monetary policy divergence with the Federal Reserve. I think in the next couple of days, Sterling will be driven by economic data rather than Brexit negotiations.

It's been a strong showing for CPI data released moments ago for the New Zealand economy. The lift to 0.5% q/q (exp 0.4%) is a strong jump and lifts y/y on inflation to 1.8% (exp 1.7%), something that is above the current Reserve Bank of New Zealand forecasts. So it certainly adds weight to the possibility of future rate rises if this can be sustained. However, there has been a lot of uncertainty creeping into the NZ economy as of late, as the election talks for the government have still not finished and markets are never a fan of uncertainty. The bigger picture though, may be the diary auction which has expectations that it could be a repeat of last week and drop. This would in turn cause disruption in the NZ economy which is heavily reliant on the dairy market and the income it generates through Fonterra. So with that, traders will be watching for the volatility and wondering if we can see a repeat of last week where the NZD was one of the most volatility currencies.

For me the NZDUSD continues to be bullish in the short term as the USD fails to strengthen at present. After touching support today at 0.7166 it has bounced higher and is looking to target the key level of resistance at 0.7219, further extensions in the short term could go higher to 0.7262 as well. The 200 day moving average is also acting as strong support in the market and helping to stop any bearish movements lending further weight to the bullish movements higher. However, if we did see a move lower on the charts the bulls are likely to target support levels at 0.7130 and 0.7054. With it being very unlikely that we could see further movements below the 70 cent market with a weak USD at present.

Oil has for some time been one of the bullish markets trading have been playing, and it certainly is looking set for further big moves as it holds up at strong resistance at 52.10. OPEC has called its programme a success thus far when it comes to stabilising oil prices and is looking to further extend those cuts in the interim to support current oil prices. It would be unlikely they would stop the current progress they've made given the success they've had. Nevertheless, the US continues to pump more oil than ever which does dampen the market and prospects of going higher.

On the charts oil continues to be bullish, but it's struggling at resistance at 52.10, which continues to stop further movement higher. The bears are strong around this level as they've protected it before and are looking to do so again. If we did see a break out higher then resistance at 53.70 would be the next target. However, if oil did drop on the chart then I would expect support at 50.21 and 48.73 in the long run.

The Australian dollar has taken a beating in recent trading days, as the selling in it was mainly a result of the recent NZ election which dragged on the AUDUSD. This may come as a surprise, but there is some correlation between the two when it comes to their pairing with the USD. However, this selling has now stopped and markets are focused on the CPI data due out in coming days, which will provide some strong direction. The current expectation is a big rise in CPI data from 0.2% q/q to 0.8% q/q, which would bring inflation in that 2% target. Going further above the 2% target we can expect this to raise the attention of fixed rate markets who will be looking to see if this gives ammunition to the Reserve Bank of Australia to lift rates. The economy does seem to be bouncing back so this catalyst could lead to the bulls rushing back into the AUDUSD, as it continues to look stable and lack any political risk when compared to NZ at present - which has a degree.

With all this in mind where to for the AUDUSD. Well there are two ways to look at it and a weaker USD is not the answer here. If we do see a weaker CPI result then I could see the AUDUSD whacked and pushed lower to support at 0.7729, but it shouldn't have a massive impact. On the upside if we saw a CPI reading that beat expectations and markets felt it might be sustained then I could see resistance at 07900 targeted, with long term upside potential of hitting further resistance levels at 0.8000. Either way you look at it there is potential for bigger movements in the AUDUSD and potentially the AUDNZD as well, but CPI figures will have a big impact on market sentiment for the rest of the week.

Shinzo Abe got what he wanted as he swept back into power after this weekend's elections and the USDJPY was quick to respond by losing some ground on the Monday open, as Yen bulls appeared in the market. The continuation of Abenomics will be interesting, it has been one of the greatest economic experiments of its time. The reality though is that it has not really caused the expected result and may have created more problems. Markets however are expecting that the Bank of Japan governor will be replaced and another more hawkish governor could be brought in to create further change from a monetary policy point of view.

For the USDJPY traders it's a good time to be bullish, but also realise that the USDJPY does like big levels and to move sideways from time to time as well. Resistance at 114.258 thus far has been a hard ask for the market and I am expecting to see a real test here. If we can see a push through then further extensions to 115.322 are likely to be on the cards here. But USD strength will also need to hold up and it has suffered recently.

The Australian dollar was thumped by the market today as CPI data missed the mark coming in at 0.6% (0.8% exp) leaving the market with a bitter taste in its month. On the back of higher oil prices and retail prices many had expected to see inflation lift and even hit the magic 2% inflation figure which might prompt the Reserve Bank of Australia into action. Sadly, it was not meant to be and the weaker figure coupled with global sentiment of weaker inflation in the mid range term means it's unlikely the RBA will get to raise rates anytime soon. So where to for the AUD? Well with the US government pushing its tax reform this could certainly boost the possibility of increasing US GDP and the USD for the most part. There has been a lot of weakness for the USD recently and that has boosted things, but for the most part it does seem realistic that they might be able to get it through. This would obviously play out well for the AUDUSD bears, especially if we continue to see weaker data in the long run.

So far the AUDUSD bears have slashed down the charts at a blistering pace before hitting the 200 day moving average coupled with support around 0.7687 and pausing for a breather. Given the recent weakness in the commodity currencies I would not be surprised to see further falls down to the next level of support at 0.7624. Nevertheless, the AUDUSD does have a habit of bouncing back, so in the event it did I would expect the potential for it to modestly rise to 0.7748, but it would be hard pressed to get higher to resistance at 0.7821. In any case I do believe that the bears may hang around for some time yet and market traders are likely to target key support levels until they find any hope for the AUD.

The UK has always been struggling with the recent Brexit negotiations but thus far FTSE 100 traders have managed to avoid the brunt of it. Not to so much today as global equity markets took a big tumble, despite growth forecasts being upgraded in the US. Markets at the moment seem quite skitterish and we are starting to see long candles, which means traders are getting very aggressive to defend these bullish positions at times.

The FTSE 100 is a fantastic case of this as we saw an aggressive dive today, followed up by some aggressive buying shortly after to bring it back into line. Support was touched at 7436, but traders were quick to defend this level, but the bears still took considerable ground. The 200 day is moving up the chart and if we break through support at 7436 then I would expect an extension further down to this level. Resistance levels can still be found at 7551 and 7600, with the potential to breakthrough looking very remote at present.

Currencies stay range bound ahead of Fed’s decision

It is a quiet Wednesday in the currency markets. Traders are favoring to remain on the sidelines ahead of multiple key risk events, including the Federal Reserve monetary policy decision later today; the Bank of England’s rate decision on Thursday; President Trump’s nomination of the next Fed Chair; the U.S. tax reform announcement and Friday’s NFP report.

Today’s FOMC meeting will not be accompanied by an update on economic projections, nor by a press conference. Traders have to act on very few amendments on a 500 words statement. The main theme is unlikely to change, and the Fed will stick to its plans of gradual tightening. However, recent economic releases have shown significant improvement in the U.S. economic activity, and GDP has grown 3% for two consecutive quarters, suggesting that we may see slight, positive changes in assessing economic activity.

Despite an uptick in headline inflation in September, core CPI continued to miss estimates, and remained below the targeted 2%. Thus, I expect little to no change on inflation assessment.

Overall, the Fed will likely meet market expectations, by keeping interest rates unchanged in November, and signal a rate hike in its final meeting in December.

President Trump’s nomination for Fed Chair on Thursday could easily overshadow today’s statement, especially if Fed Governor Jerome Powell is not his first choice. Powell has been supportive of Janet Yellen's policy of gradual tightening in monetary policy; thus, I do not expect big moves in Treasuries, or the U.S. dollar, if he is nominated. However, if Stanford University’s Professor of Economics, John Taylor, is nominated instead, expect big moves in Treasury yields and the dollar, which could appreciate sharply against its peers. According to Taylor rule, a forecasting model that determines where interest rates should be, based on targeted inflation and full employment, interest rates should be much higher the current levels.

The Kiwi was the only outperforming currency today, surging 1% against the dollar after labor market statistics showed that the cost of labor grew 1.9%, and the unemployment rate fell to a nine-year low. If wages continue to show signs of strengthening, the Reserve Bank of New Zealand will likely start raising rates next year, as opposed to earlier forecasts of tightening in 2019.

The build up has begun for tomorrows NFP announcement and the market is betting big time on a strong result of 313K; this is a very large expectation, but it makes a lot of sense when you consider the seasonal impact that Christmas has on markets. Labour markets certainly boom during this period and even part time workers are considered part of the work force. I will say one thing, with such a large number it will be hard to beat, and I'm not certain that markets will take kindly to anything below the 313K, so it could be the NFP of the year on this basis. Markets will also be digesting the recent announcement that Powell will take over from Yellen as the FED chair. The markets thus far have been positive regarding this, with a number of heavy weight finance figures speaking out in favour of him. Many had expected a hawk, but the reality is that he's likely to take over from the Yellen framework and continue it in the short to medium term until he has a good grasp of the situation.

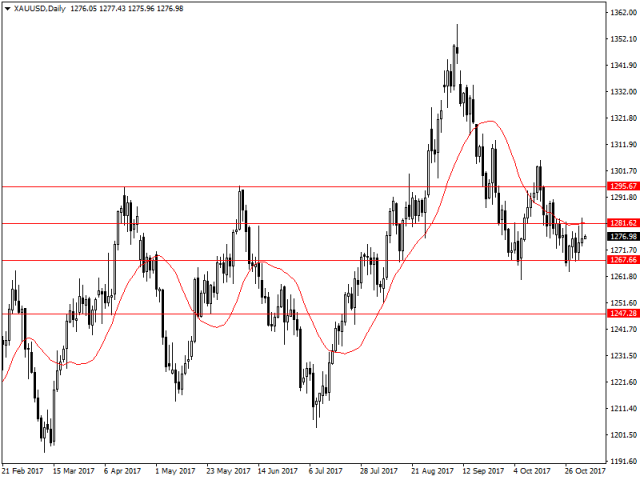

For the NFP traders, the metal markets is always the big calling when it comes to movements. Gold has thus far been creeping up on whatever USD weakness it can find, which is not surprising as the bulls are always there. Any NFP weakness tomorrow could see gold catapulted above the current resistance level at 1281 with the potential to even break through 1295 if it's quite bad. In the event it's a very strong result and in line with expectations then 1267 and 1247 are likely to be key levels of support for the gold market. All the moving averages at present are not likely to impact any shifts upwards or downwards so it will be a case of playing of key price levels that the market can digest at this present time.

It was also a big day for the British market as the Bank of England raised interest rates by 25 basis points, leaving the intraday banking rate at 0.5%. This move had been widely expected, but the comments afterwards helped drive the pound down and encourage the doves in the market as the Bank expected inflation to taper off (as the pound stabilised) and also Brexit would bring uncertainty to the market causing issues in the long run.

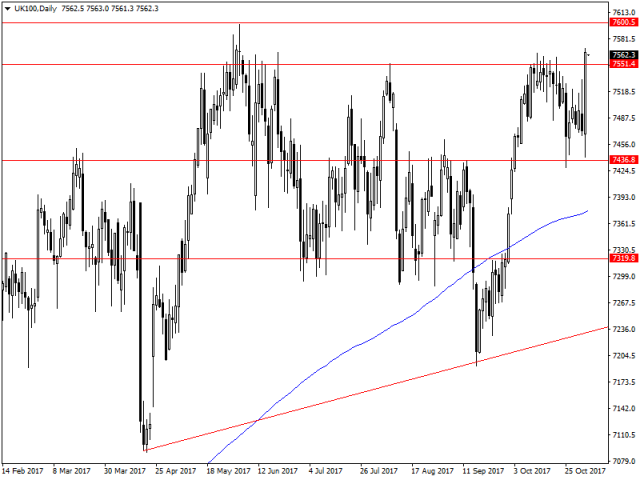

The big benefactor of this was of course the FTSE 100 which lifted sharply on the news as the bulls rushed in to take advantage, and as the UK oil producers showed strong earnings as well. The market is now poised to have another crack at resistance at 7600 and NFP could be a catalyst which could push it through tomorrow as well. In the event that markets fall back down support at 7551 and 7436 is likely to be key levels, and markets will be looking to stop the rot if anything does transpire.

The New Zealand government continues to be in the eye of traders as the current changes to the Reserve Bank of New Zealand look to be fast tracked. So far what we know is that the focus will not only be on inflation, but almost full employment for the NZ economy. This should come as no surprise given the recent elections and the want for the government to change to focus on this. Additionally, there is the need for a change on current FX policy which could have far reaching impacts on the NZ economy, as the current minor party (NZ first) wants to see the RBNZ intervene in FX markets to help drive export markets and keep the NZD lower. This has been seen as futile in the past given the RBNZ being quite small compared to world markets, so it could cause minor issues going forward. Either way markets are not currently upbeat regarding the prospects of the NZDUSD, but I believe the NZD is starting to stabilise compared to other currencies and is showing the odd signs of the bulls back in the market.

So far the NZDUSD bull have managed to claw back a considerable amount of ground in the face of uncertainty in the NZ economy. For me resistance at 0.6960 is the current strong level that is holding back any further gains on the charts, the reason being is that no one knows the current direction of the NZ market after elections. If it was positive then I would expect a jump to 0.7029, but a potential slow down shortly after this jump. In the event we did see minor falls on the charts then support could be found at 0.6891 and 0.6834 respectively, with the ability to go lower as markets are considerably more bearish after the recent election.

Oil has been one of the big jumpers on the charts as markets have been quick to worry about the situation in Saudi Arabia recently. The anti corruption crackdown has taken a few high profile heads, and the markets are worried about the state of play from the world's largest oil producer. Certainly, there have been drawdown's on global oil supplies, but the shakeup of affairs could have the largest impact in the long run and drive oil prices higher in the short term.

So far Oil bulls have charged forward and knocked out support at 56.17 as the oil markets continued to run higher. Resistance level can be found at 59.08 and 62.12 on the charts with the potential to go higher if more political uncertainty presents itself. There is also the potential for charts to dip lower and support can be found at 56.17 and 50.21 as the market looks to drift lower as news looks more promising potentially.

The Euro has been a star over the previous months, but it's becoming more and more lacklustre as the ongoing Spanish drama is still a thorn in the side of the Euro-zone. While investors love a bit of volatility, the Euro-zone seems to keep battling crisis after crisis trying to hold everything together as more moles pop every month to be whacked. Is there cause for concern? Well markets seem to think so as of late, and event EU retail sales figures y/y jumping to 3.7% (2.8% exp) were not enough to fight of the bears. Additionally, the US saw a strong JOLTS job openings figure of 6.09M (6.08M) which shows that the labour market in the US continues to not be at capacity. This can also be seen in the fact that wages have not grown as fast as economists had expected, which points to slack in the labour market that can still be filled. It would seem though that we are close capacity in the next year or two in the US if there are no negative economic events.

So for the Euro bulls it's been a tough ride over the past few weeks and the head and shoulders pattern that did occur is likely to keep going with bears taking full advantage. Target support levels for the market will be found around 1.1519 and 1.1433, with the potential for further lows if we see any further weak news on Catalonia. If we do see the bulls come back into the market I would expect to see resistance be strong around 1.1621 and 1.1719 on the charts. Additionally, the 20 day and 50 day moving average should be watched as dynamic resistance levels which daily traders have been respecting as of late. However, for the most part there is a clear trend of bearish sentiment which has the potential to continue for some time.

NZ dollar traders also went short today as the Global Dairy Index came in at -3.5%, obviously this is quite big news for traders as the Dairy industry accounts for 7% of New Zealand's GDP. But further to this we have the RBNZ rate statement due out tomorrow, and many are expecting some fireworks here. Not in the sense of a rate rise, but in the sense that change is in the wind with the new government wanting it to have stronger mandates. It will be a case of wait and see, and the prospect of a new governor is on the cards as well with the new left wing government.

For the NZDUSD traders there has been a failure to breach anything above the 70 cent market, which continues to act as a psychological barrier at present. Markets thus far are looking bearish and swinging lower just coming up short of support at 0.6891. There is further potential for moves lower to 0.6834 and 0.6802 on the charts. I would be surprised to see it spring back up higher, but if it does the 70 cent mark is likely to be a hard stop for the pair.