The pound has come under increased pressure over the last few weeks, as the so called Brexit continue to fail to come to any sort of conclusions at all for markets. Certainly there is a case for leaving the EU, however no politicians can come to any sort of agreement on it. Further to the downside has been UK retail sales m/m coming in at -4.2% (-0.75% exp), which is much worse than anyone expected, and a figure not seen since 1995 when records began. It's clear that off the back of this traders will be looking to offset losses and clear balance sheets.

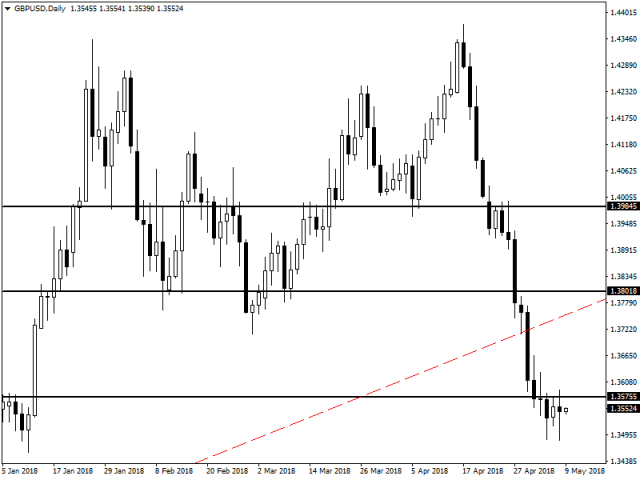

Looking at the GBPUSD it's clear to see that that the daily char reflects a number of key points, the first being that Brexit continues to be a major topic and that the initial positivity of a quick solution has quickly failed. Further to this economic data continues to be a mixed bag as can be seen from the retail sales figures above, which will put further pressures on UK businesses. For me the defining technical movement is of course resistance at 1.3575 holding up very strongly to any pressure at present and preventing anything but bearish movements from happening. The market as a result is looking increasingly like it may look to move lower to support at 1.3314 if the bearish pressure continues in the short term. However, a push down here may provoke a very strong bearish pressure.

The Australian dollar can get no breaks as of late, as it continued its bearish run against the USD even further today. This comes as no surprise as the trend has been quite bearish, but also retail sales m/m came in at 0% (0.2% exp), showing that the consumer sector is weaker than expected. While not largely off the market it continue to show that the Reserve Bank of Australia will struggle to lift rates in the near future if the status quo continues.

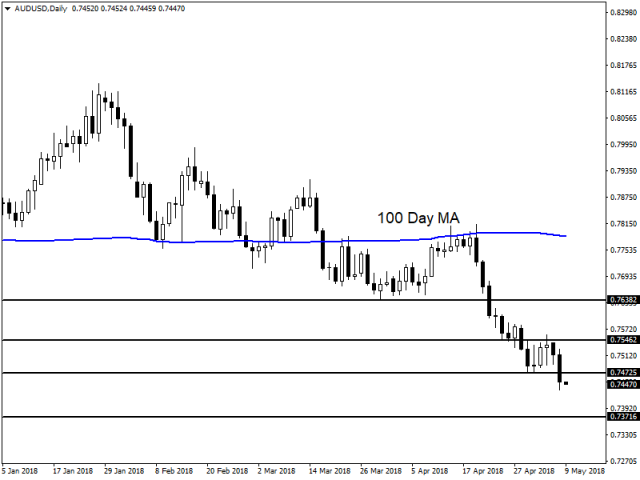

Looking at the AUDUSD on the charts it's clear to see the bearish trend that has been in effect for the last month and looks set to continue in these circumstances. The AUDUSD has cracked through support at 0.7472 and is now looking lower on the charts in the face of bearish pressure, to the potential support level at 0.7371 as the bears look to target lower lows. In the event we do see any bullish pressure in the market expect 0.7472 to be the key area that will either allow the bulls to take control or reaffirm the bearish trend in this market, as the AUDUSD continues to be a bearish story in the interim.

Daily Fundamental ForexTime ( FXTM )

AUD struggles in market enviroment

The Australian dollar got some positive news for a change as it faced off against the USD and won a round for the bulls after a month of bearish pressure. This has been positive on the fact that the Australian economy in the employment sector has performed better than most expected with Australian employment coming in at 22.6K ( 20K exp) and the unemployment rate lifting to 5.6% (5.5% prev) on the charts as a result. For now the Australian dollar continues to find itself under pressure, with the labour market being the only strong point. Despite all of this the Reserve Bank of Australia continues to look for positives for the future, with inflation being a key compontent for any future rate rises.

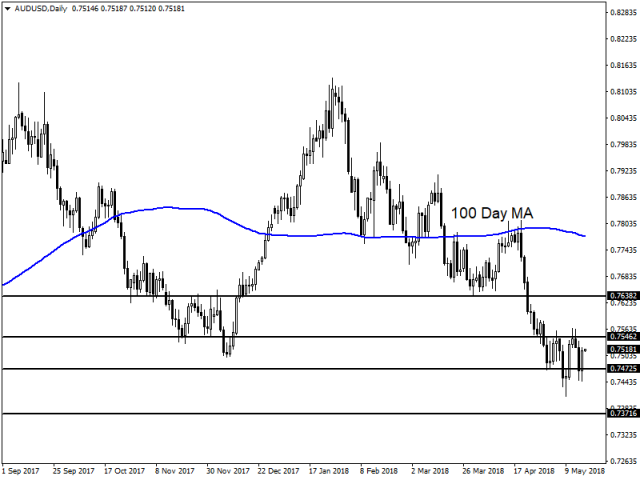

The AUDUSD continues to climb high, but only on the back of weaker currencies as of late. The AUDUSD failed to make it through resistance at 0.7506 as traders are quite bearish above that level of pace that the AUDUSD continues to go through. Traders will be looking ot see if the market can indeed pressure here and breakthrough, but in reality it could be another bearish test followed by further pressure on 0.7472. I would expect in the long run that we could potentially see an extension to 0.7371 on the charts if the USD strength continues to be a mainstay for the market. All in all the AUDUSD finds itself in a unique position and I would expect to see further bearish pressure unless anything radical comes about in the markets.

The other key mover has been EURUSD which has struggled to find its feet under immense pressure from the USD but also weakness in Europe surronding Iran and Italy. The market has been looking for strong words from the EU and how much the Italian goverement changes will influence the EU, but so far it has shown little promise of anything radical in the way of changes. Despite all of this the EURUSD is always a favourite for traders and has slid down the charts reflecting USD strength. If we do see futher politiacl pressure we could see the EUR drop further against all major pairs.

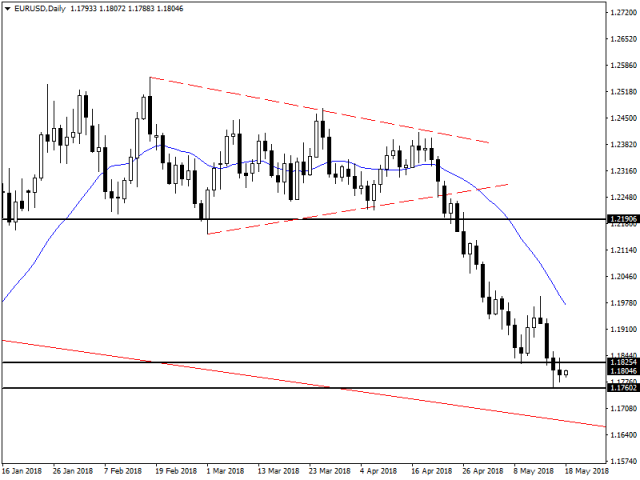

One of the key areas has been support has been 1.1760 which has so far defending againt any and all bearish movements lower on the charts. It's unlikely this key level will hold in the long run and we could see further slippage down into the low 1.10 levels if the USD strengthening continues. I would expect that any movements higher are likely to find strong resisstance at 1.1825 on the charts as this level has come under pressure in the past.

Asian stocks gained on Monday morning as investors learned that the U.S. and China agreed to drop the tariff threats against each other while they continue to work out an agreement. This was the second round of trade negotiations without clearly defined targets, suggesting that there’s still a long way to go. Today, a trade war may have been averted, but according to the joint statement from both countries, nothing is being guaranteed apart from China promising to increase American imports. It seems that tensions will remain for the foreseeable future and investors will have to live with it; unless the U.S. officially announces that it is imposing tariffs on China, the noise in the background will have little impact on sentiment.

Nicolás Maduro wins Venezuelan elections

As was widely anticipated, Nicolás Maduro won another six years in office in Sunday’s elections. The Venezuelan economy, which has been struggling for several years, may enter a deeper crisis if the U.S. and other western countries step up sanctions against the nation. Brent crude, up 0.7% at the time of writing, might benefit further from the increasingly grave outlook for Venezuela, if proposed sanctions result in a steeper decline in output.

FOMC minutes

The dollar climbed to a new 2018 high on Monday, with overall gains of more than 6.3% from its lowest point in February. The U.S. currency has been benefiting mainly from improved economic prospects and higher interest rates. Whether the upward trajectory will resume in the short run, is likely to depend on the FOMC minutes scheduled for release on Wednesday. The Fed has changed its language with respect to inflation and become slightly more bullish, but its latest statement didn’t indicate a faster tightening in monetary policy. Whether the Fed is prepared to fight inflation, or whether it will be more cautious about raising rates too quickly, will be reflected in the minutes. However, with a number of speeches scheduled from Fed officials this week, it will be interesting to hear their thoughts on how oil above $80 may impact policy.

Italy’s new government

Italy's new government is likely to be formed within the next few days and provide a new headache for Brussels, since populists will be leading it. Italian borrowing costs rallied sharply over the past several days, as investors sold Italian debt after a leaked draft showed the new coalition’s intentions to request the cancellation of €250bn of Italian government debt. How things go from here depends on whether the new government follows through on its promises, that include a massive spending spree that conflicts with the EU’s budgetary rules, or whether it starts to gradually scale back .

FOMC minutes were released not too long ago and they reveal that the June rate hike is very likely to happen after FED members were positive about the state of the economy and the recent rise in inflation. It also showed that if inflation did increase beyond forecasts they FED would likely let it run instead of risking bumping rates to soon and causing a pinch effect in the economy if it tapered off; as a result the USD is a little weaker as many had expected the FED to be more hawkish, rather than let inflation run in this instance. The FED also noted the recent risks, with China and NAFTA being threats to the US economy and progress overall for the expansion of the economy. However, there is little the FED can do but try and negotiate the turbulent waters that come with politics and trade agreements.

One of the big movers on the back of the USD weakness has been of course the USDJPY, which moved quite heavily as a result of bad economic data (US home sales) and of course the dovish response from the FED in regards to inflation.

The USDJPY had been moving in a tight channel up the charts as the USD appreciation and positive risk sentiment saw traders looking to exit the USDJPY. However, after today's movements that channel has now been broken and even a bullish fight back was unable to contain the bears as they looked to swipe a little lower. Traders may be looking now to target key support at 109.347 and with further potential falls to 107.718 on the cards as well, but it's also worth noting that the USDJPY does not break levels easily and can just as easily move sideways until it finds direction. In the event this is just a pause I would look for markets to have another crack at resistance at 111.083. The long term for the USDJPY does look to be bullish, but the positive risk climate must continue to enable it to do so, and there will inevitably be days where these sort of movements happen.

The other back mover made reference to by my colleagues has been of course the Turkish Lira which has come under immense pressure over the last few days, as a strengthening USD and economic/political factors have undermined the currency heavily - much like the Russia crisis a few years ago.

The Turkish Central Bank has taken the extraordinary step to intervene without any formal meeting, lifting interest rates by 3% in the wake of all the aggression. This has had a positive effect when it comes to stopping the bleeding for the currency, as it touched on resistance at 4.9200 but has since fallen back sharply since the rate rise. Markets will now be looking for potential support levels, but it's hard to tell where they start and stop with possible areas being at 4.4916 and 4.2840, if the bears continue to fight back.

CAD lifts on rate rise prospects, EUR also in focus

The Canadian economy has been the big talking point of this afternoon with the Bank of Canada (BoC) keeping rates flat at 1.25%. The major change though was the removal of dovish wording from the monetary policy statement, and now starting to align that wording with their American counterparts the Federal Reserve. The odds now of a hike at the next meeting in July have increased drastically as a result and this should not come as to much of a surprise, given that inflation has been running at 2% recently which gives the bank the mandate to look to move rates higher from the artificial lows they've been sitting at for some time. The only thing that could derail things is upcoming GDP figures which are expected to be slightly weaker, though analysts may change this in the wake of the Bank of Canada's confidence, and NAFTA - which continues to drag on with the US and Mexico. However Canada has said it won't cut a deal which negatively impacts Canada's main industries.

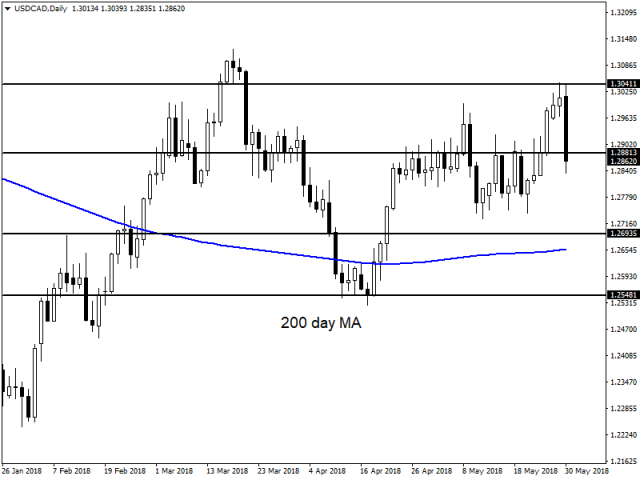

For the USDCAD some serious movement has taken place and the bears were quick to capitalise on the USD sell off today and the CAD's strength. So far the USDCAD has moved below the 1.2881 level on the charts and if it can remain below this support level we could see some further selling pressure and potentially a move to 1.2693 on the next leg. At the same time if we close above this key support level then potentially it's a sign that the bulls think the USD still has plenty in the tank to run with and we could see another leg back up to 1.3041. All in all, it's looking quite bearish, and we could get another few days on the back of the BoC announcement.

The other major talk of the town today was the complete U-turn in Italian politics. With the President and PM coming together to allow more time for the government to set up its coalition, and also the 5 star movement asking that Savona not be nominated for the finance/eco minister role for Italy. This of course still has its challenges, but at the same time it removes a major euro sceptic from a key position in the goverement and euro bulls were quick to rally as a result. There are a number of challenges ahead, but at the same time it could in theory lead to a more stabilised, yet progressive Italian government, that won't be so aggressive towards the euro-zone.

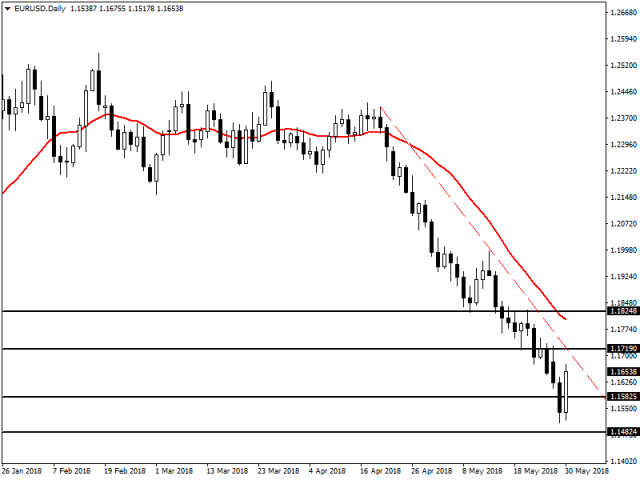

The EURUSD as a result has rallied strongly eclipsing all of yesterday's losses, but has failed to capitalise on the follow days candle. This to me is a strong sign that perhaps markets are positive but being cautious here. Resistance at 1.1719 will be interesting, with markets likely to look for some sort of political relief before extending further to the next level at 1.1824. At the same time if the bears are serious in the market, they may look to jump on the news and push the Euro down to 1.1482 in the long run.

Trade war fears to dominate market moves this week

Intense G7 meeting

After imposing tariffs on steel and aluminum imports on its closest allies, the U.S. will be facing enormous criticism at the G7 summit on Friday in Quebec or, as the French Finance Minister Bruno Le Maire likes to call it, “G6 plus one.”

“When you’re almost 800 Billion Dollars a year down on Trade, you can’t lose a Trade War! The U.S. has been ripped off by other countries for years on Trade, time to get smart!” Donald Trump

Whether President Trump is playing a smart strategic game or is seriously considering getting into a trade war remains unknown, but the probability of a full-blown trade war has undoubtedly increased significantly.

The summit is due to take place after the U.S. and China trade negotiations ended on Sunday without any significant progress made. In fact, China warned the U.S. that any move to implement tariffs on Chinese products would ruin the negotiations.

Although markets in Asia are rallying after the U.S employment report released on Friday showed a robust surge in numbers and new elections were avoided in Italy, this optimism will soon disappear if the Trump administration pulls the trigger on the threatened tariffs on $50bn worth of Chinese exports. So, keep a close eye on Trump’s Twitter account for updates.

Europe’s Politics and data to be in focus

The Euro struggled last week, with Italian and Spanish political turmoil sending the single currency to its lowest level since July 2017. The compromise reached between the Italian President and the populist coalition prevented further losses as a new election seems to be off the cards for now. This relief was reflected in Italian bonds where 2-year yields fell 200 basis points from Tuesday’s high. However, the Euro’s recovery may be short-lived if the new Italian government moves ahead with its proposed massive spending agenda and tax reductions. These actions will not only create conflict with Brussels but will also invite credit rating agencies to cut their debt ratings.

On the data front, the Eurozone Services PMI is likely to confirm that the economy continued to slow down as it entered Q2. Another round of negative economic releases will lead the ECB to postpone ending QE and thus drag the Euro further. The UK services PMI, Germany’s industrial production and factory orders will also be in focus this week.

Oil markets have suffered another blow today as US oil inventories showed an increase of 2.07M barrels (-2.1M exp), while at the same time US gasoline inventories also showed a strong increase to 4.6M (0.5M exp). This has come as a bit of surprise for the market which had been expected drawdown's and probably more so for OPEC and its allies, as they look to ramp up production to find an equilibrium and maximize profits from the high oil price we have at present. Certainly the OPEC meeting due out on the 22nd of June will be very interesting, where it is expected that Saudi Arabia and Russia will continue their ramping up of prices. Many are expecting that with Iran out of the picture this does give the Saudis and Russia the chance to put production up even if the price if oil is not doing well.

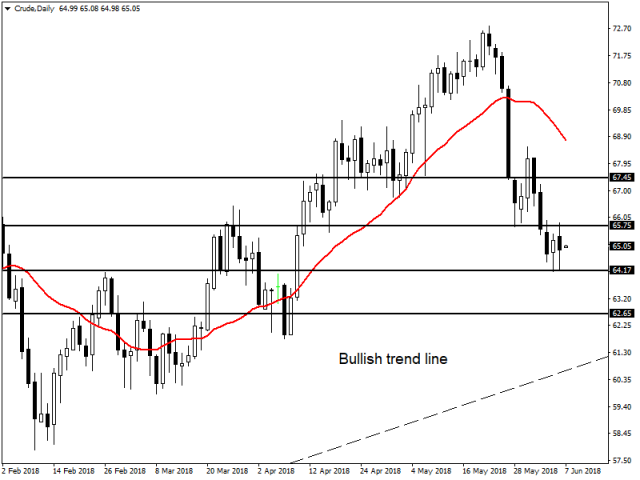

On the charts it has been very bearish for oil as of late. So far we saw a peak for oil at 72.81, followed by oil falling back down to earth in a hurry - not surprising given that oil trending very hard, and it does not always continue. This bullish buy hit resistance at 65.75 when trying to claw back some ground against the bears and it really does look like it may struggle to breakthrough this level in the interim. For bearish traders feasting off the data the next levels of support can be found at 64.17, with the potential to extend even lower to 62.65 in the long run. I would also focus on the long term potential trend line as well, which could propel oil to something further in the long. Looking at the bulls however resistance as mentioned above can be found at 65.75 and 67.45 in the long run, but it may take some cracking to get them through given the OPEC meeting.

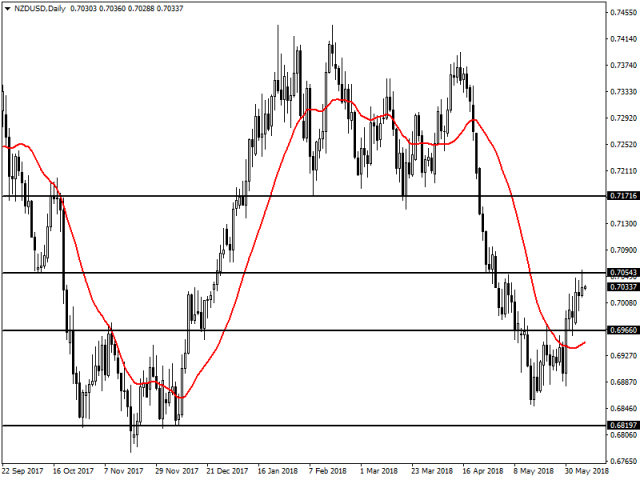

One of the other key winners today was the NZD which enjoyed the risk sentiment of the market as it started. So far the despite positive data the US market has enjoyed, it has translated into more foreign investment outside the US in other currencies and the NZD and AUD were no exception today.

Looking at the charts we can see that the NZD has cracked through the important 70 cent barrier mark and is climbing higher, but has stumbled against resistance at 0.7035. With bullish traders looking to assert themselves it would seem that the NZDUSD could end up taking on the next level of resistance at 0.7171 if the bulls stay in control. On the flip side support still remains at 0.6966 and 0.6819 in the long run.

Global stocks have bounced back to life after China’s central bank calmed markets by urging investors to “stay calm and rational”.

While this move by the People’s Bank of China (PBOC) could support risk sentiment and push equity markets higher in the short term, gains are likely to be limited. With trade war fears still a recurrent market theme that continues to weigh on sentiment, investors may start questioning the sustainability of the stock market rally. Markets are likely to remain cautious with any signs of escalating trade tensions between the United States and China potentially sparking a renewed wave of risk aversion.

Bank of England policy meeting in focus

Today’s main event risk for the British Pound will be the outcome of the Bank of England policy meeting, which is widely expected to conclude with monetary policy left unchanged.

With the BoE expected to keep interest rates on hold, investors will most likely closely scrutinize the policy statement and MPC vote count for insight on rate hike timings beyond June. The Pound could weaken if the central bank expresses concerns over Brexit related uncertainty and political risk negatively impacting growth. Pound weakness may remain a dominant market theme if Brexit uncertainty results in the BoE repeatedly delaying monetary policy normalization.

Taking a look at the technical picture, the GBPUSD is bearish on the daily charts. The solid daily close below 1.3200 could invite a further decline towards 1.3130 and 1.3100, respectively.

Currency spotlight – Dollar

The Dollar has scope to extend gains against a basket of major currencies amid market expectations over the Federal Reserve raising US interest rates at least two more times this year.

Away from the fundamentals, the technical picture remains heavily bullish with prices hovering near an 11-month peak as of writing. There have been consistently higher highs and higher lows, while prices are trading firmly above the 200 daily Simple Moving Average. A firm daily close above the 95.00 level could open a path towards 95.35 and 96.00, respectively.

Commodity spotlight – Oil

There is a growing sense of uncertainty mounting ahead of Friday’s OPEC meeting, with markets now re-evaluating if an output increase could still be on the table.

While Saudi Arabia and Russia are pushing OPEC and its allies to raise production, other members including Iran, Iraq, and Venezuela have opposed such a move. With Iran already stating that it was likely to reject any agreement that raised output, this could be a fractious meeting between oil producers in Vienna. Whatever the outcome of the OPEC meeting, it could have a lasting impacting on oil prices.

Pound comes under pressure after Brexit resignations

The Pound has been in the spotlight today after two cabinet resignations of key Brexit leavers shook the Tory government up. What some were calling a political crisis seems to have subsided so far, and the markets will be looking to see how the new appointments handle the outgoing ministers and if they can bring anything new to the table. However, all the uncertainty drags on the pound and the drop today was mainly on the back of Boris Johnston's resignation, as he has been a key vocal enemy of any soft Brexit. Regardless of the politics the UKs government remains deeply divided over the customs union and the Irish border, and it seems ever likely that they will be forced to potentially ask the EU for an extension if things don't progress much more rapidly. For the Pound this could mean heavy pressure in the coming months, but for now the bulls are doing their best to stave off the bears.

Looking at the GBPUSD in particular and it's clear to see that the bulls are trying to push it away from the bullish trend line and back up, as the USD stalls on its epic run of late. Bullish traders will now be looking to aim for resistance at 1.3432 on the charts, with the potential to go further higher if they can get some positive Brexit news. In the even though that we do see the bears flood back into the market, then I would expect strong pressure on support levels at 1.3171 and the trend line just below that, which will act as dynamic support. For all it's worth though GBPUSD traders are likely to be short term holders though in the current market environment so I would expect plenty of whiplash in the markets as they pivot on news from the media.

Good and bad news out the US today as US consumer credit has lifted to 24 billion (12 billion exp) for this month. This is the largest deviation since 2016 and the markets will be looking to see if it's a pattern that will continue or it's just US consumers enjoying the summer season. Equity markets on the consumer side will be the most affected at this stage I feel as US consumable companies will benefit the most from the tax benefits and also US consumers spending far more.

After support was found at the 100 day moving average the S&P 500 has benefited greatly from a bullish run coming up just short of resistance at 2787, if market conditions continue we could see a further push to 2835. In the event we see some bearish pressure I would expect support at 2741 to be the first candidate followed by the 100 day moving average acting as dynamic support. However, what might be the most curious will be when the 100 day and 200 day moving average cross, and how markets react to this technical signal. For now though the bulls are in charge of the market.

Emerging market currencies have been treated without mercy by a broadly stronger Dollar, yet again.

The Dollar Index appreciated to its highest level this year above 95.50 due to heightened expectations over higher US interest rates this year. The Chinese Yuan, Malaysian Ringgit, Indonesian Rupiah, Singapore Dollar and most other major EM currencies have all felt the heat. With Dollar strength likely to remain a dominant market theme and global trade tensions negatively impacting risk sentiment, EM currencies appear destined for further punishment.

In regards to the Chinese Yuan, price action continues to suggest that the local currency remains heavily influenced by external forces. With the Yuan already weakening to a fresh yearly low, further losses could be expected amid an appreciating Dollar. Taking a look at the USDCNY, a decisive daily close above 6.750 could inspire an incline to levels not seen since June 2017 around 6.810

Dollar bulls are back in town

It has certainly been an incredibly positive trading week for the Dollar.

Federal Reserve Chairman Jerome Powell’s bullish testimony could be one of the primary drivers behind the Dollar’s appreciation, especially when considering how he reinforced expectations of higher US rates this year.

Taking a look at the technical picture, the Dollar Index has scope to venture towards 96.00 and 96.40 if bulls are able to secure a daily close above 95.00.

Commodity spotlight – Gold

Gold is poised to conclude this week in heavy losses thanks to an appreciating US Dollar.

The yellow metal remains under intense pressure on the daily charts with prices trading marginally below $1220 as of writing. With the combination of Dollar strength and prospects of higher US interest rates eroding appetite for the zero-yielding metal, Gold is firmly bearish. Sustained weakness below $1200 could inspire a decline towards $1209 and $1200, respectably.