FXTM Official

Active Member

- Messages

- 1,156

- Joined

- Mar 12, 2013

- Messages

- 1,156

- Reaction score

- 2

- Points

- 25

Forextime.com Daily Market Analysis

Dollar sensitive ahead of US retail sales

The fluctuating expectations over the Federal Reserve raising US interest rates in 2016 have left the Dollar in a sensitive state with prices violently oscillating between losses and gains. Conflicting data this month such as the firm NFP and soft labor productivity have trapped the Dollar in a fierce tug of war with anxiety mounting ahead of Friday’s retail sales. Retail sales could offer investors a rough idea on consumption and GDP in the US economy with a positive figure potentially dispelling this period of Dollar sensitivity. Overall the sentiment towards the US economy is turning bullish and markets have already priced a 50% chance that the Fed could raise US rates in December.

From a technical standpoint, the Dollar Index is trapped below the stubborn 96.00 resistance, but a breakout above this level could open a path towards 98.00.

Sterling bears take no prisoners

The heightened expectations over the Bank of England cutting UK interest rates to near zero to reclaim economic stability has caused Sterling vulnerability to become a recurrent theme in the currency markets. Sterling has been placed under extreme pressure as the combination of soft domestic data and post-Brexit uncertainties have encouraged sellers to incessantly attack. The GBPUSD tumbled to a fresh monthly low on Thursday and could trade lower in August if the divergence in monetary policy between the Fed and BoE encourages investors to install another round of selling. Uncertainty is still a dominant theme which has haunted investor attraction towards the Sterling consequently obstructing any upside gains.

From a technical standpoint, the GBPUSD is bearish as there have been consistently lower lows and lower highs. Prices are trading below the daily 20 SMA while the MACD has also crossed to the downside. Previous support around 1.3100 could transform into a dynamic resistance that opens a path lower towards 1.2800.

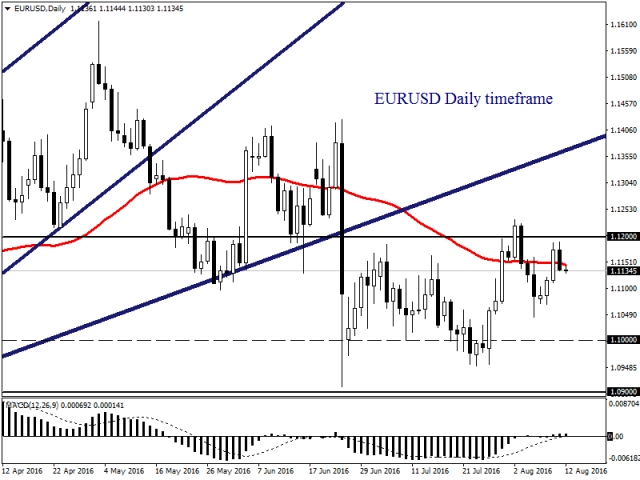

Eurozone still pressured

The shockwaves caused by Brexit have heavily punished the Eurozone with current outlooks looking tepid as uncertainty weighs on sentiment. Eurozone growth in Q2 unexpectedly halved while optimism over the European Central Bank boosting inflation continues to diminish. Amid the fears of the European economy eroding, expectations have risen over the European Central Bank implementing further stimulus measures to jumpstart growth. Sentiment is bearish towards the Euro with investors potentially exploiting the divergence in monetary policy between the ECB and the Fed to send the EURUSD lower. The EURUSD bulls have struggled to break above 1.1200 regions and if this resistance defends then bears could pounce sending prices lower towards 1.1000.

WTI Crude elevated by OPEC

WTI Crude surged ferociously on Thursday with prices edging towards $44 after Saudi Arabia discussed the possibility of hiking prices at September’s informal meeting. Oil prices have become increasingly sensitive to production freeze talks and this continues to create speculative boosts in prices. Regardless of these short term gains, WTI remains fundamentally bearish with the ongoing oversupply concerns haunting investor attraction. If the informal meeting in September concludes without a solution to the excessive oversupply, then this current relief rally could offer an opportunity for bears to drag oil lower. From a technical standpoint, previous support around $44.50 could act as a dynamic resistance which attracts sellers to send prices lower towards $41.00.

Commodity spotlight – Gold

Gold displayed erratic characteristics during trading this week from Dollar sensitivity and fluctuating US rate hike expectations. Although risk aversion and ongoing concerns over the global economy have kept the precious metals buoyed, the sharply appreciating Dollar continues to hammer prices lower. If US retail sales exceed expectations today, then Gold could be left vulnerable to losses as a combination of Dollar resurgence and renewed hopes of a US rate hike entices bears to attack Gold. From a technical standpoint on the daily timeframe, this yellow metal does fulfill the prerequisites of a bullish trend as there have been higher highs and higher lows. Bulls still have some breathing room above $1315 but a breach below this support could suggest that bears are back in action.

By Lukman Otunuga, Research Analyst

Dollar sensitive ahead of US retail sales

The fluctuating expectations over the Federal Reserve raising US interest rates in 2016 have left the Dollar in a sensitive state with prices violently oscillating between losses and gains. Conflicting data this month such as the firm NFP and soft labor productivity have trapped the Dollar in a fierce tug of war with anxiety mounting ahead of Friday’s retail sales. Retail sales could offer investors a rough idea on consumption and GDP in the US economy with a positive figure potentially dispelling this period of Dollar sensitivity. Overall the sentiment towards the US economy is turning bullish and markets have already priced a 50% chance that the Fed could raise US rates in December.

From a technical standpoint, the Dollar Index is trapped below the stubborn 96.00 resistance, but a breakout above this level could open a path towards 98.00.

Sterling bears take no prisoners

The heightened expectations over the Bank of England cutting UK interest rates to near zero to reclaim economic stability has caused Sterling vulnerability to become a recurrent theme in the currency markets. Sterling has been placed under extreme pressure as the combination of soft domestic data and post-Brexit uncertainties have encouraged sellers to incessantly attack. The GBPUSD tumbled to a fresh monthly low on Thursday and could trade lower in August if the divergence in monetary policy between the Fed and BoE encourages investors to install another round of selling. Uncertainty is still a dominant theme which has haunted investor attraction towards the Sterling consequently obstructing any upside gains.

From a technical standpoint, the GBPUSD is bearish as there have been consistently lower lows and lower highs. Prices are trading below the daily 20 SMA while the MACD has also crossed to the downside. Previous support around 1.3100 could transform into a dynamic resistance that opens a path lower towards 1.2800.

Eurozone still pressured

The shockwaves caused by Brexit have heavily punished the Eurozone with current outlooks looking tepid as uncertainty weighs on sentiment. Eurozone growth in Q2 unexpectedly halved while optimism over the European Central Bank boosting inflation continues to diminish. Amid the fears of the European economy eroding, expectations have risen over the European Central Bank implementing further stimulus measures to jumpstart growth. Sentiment is bearish towards the Euro with investors potentially exploiting the divergence in monetary policy between the ECB and the Fed to send the EURUSD lower. The EURUSD bulls have struggled to break above 1.1200 regions and if this resistance defends then bears could pounce sending prices lower towards 1.1000.

WTI Crude elevated by OPEC

WTI Crude surged ferociously on Thursday with prices edging towards $44 after Saudi Arabia discussed the possibility of hiking prices at September’s informal meeting. Oil prices have become increasingly sensitive to production freeze talks and this continues to create speculative boosts in prices. Regardless of these short term gains, WTI remains fundamentally bearish with the ongoing oversupply concerns haunting investor attraction. If the informal meeting in September concludes without a solution to the excessive oversupply, then this current relief rally could offer an opportunity for bears to drag oil lower. From a technical standpoint, previous support around $44.50 could act as a dynamic resistance which attracts sellers to send prices lower towards $41.00.

Commodity spotlight – Gold

Gold displayed erratic characteristics during trading this week from Dollar sensitivity and fluctuating US rate hike expectations. Although risk aversion and ongoing concerns over the global economy have kept the precious metals buoyed, the sharply appreciating Dollar continues to hammer prices lower. If US retail sales exceed expectations today, then Gold could be left vulnerable to losses as a combination of Dollar resurgence and renewed hopes of a US rate hike entices bears to attack Gold. From a technical standpoint on the daily timeframe, this yellow metal does fulfill the prerequisites of a bullish trend as there have been higher highs and higher lows. Bulls still have some breathing room above $1315 but a breach below this support could suggest that bears are back in action.

By Lukman Otunuga, Research Analyst